The call usually comes after a rough week in the market. A client has opened the portal, seen too much red, and asked the question advisors hear all the time: what in this portfolio is built to behave differently when stocks sell off?

That question gets harder when the portfolio looks diversified on paper but not in practice. Large cap equities, small cap equities, international equities, credit, even some alternatives can start moving together when stress rises. Clients notice. Advisors notice faster, because they also have to explain why a diversified allocation can still feel like a single trade during a drawdown.

That's where long short equity hedge funds enter the conversation. Not as a cure-all, and not as a label that should be accepted at face value, but as a potentially useful portfolio tool. Used well, they can help separate manager skill from broad market direction, reduce sensitivity to equity swings, and create a more thoughtful risk budget. Used poorly, they can become expensive equity proxies with limited hedging value.

Table of Contents

- Navigating Todays Volatile Markets

- How a Long Short Equity Strategy Works

- Analyzing Return Risk and Fee Structures

- Portfolio Use Cases for Financial Advisors

- A Due Diligence Checklist for Selecting Funds

- Marketing and Compliance in a Regulated World

- Integrating Long Short Strategies Thoughtfully

Navigating Todays Volatile Markets

A familiar scenario unfolds in many advisory firms. The client isn't asking for a market forecast. The client wants to know whether any part of the allocation is designed to hold up when headlines turn ugly and correlations tighten.

That conversation often exposes a real portfolio construction problem. Many client accounts contain a sea of sameness. Different sleeves, different manager names, different wrappers, but the same underlying dependence on equity beta. In calm markets, that overlap stays hidden. In volatile markets, it becomes obvious.

Why the client question matters

Clients usually aren't asking for complexity. They're asking for behavioral clarity. They want to know what should happen if markets fall, where the portfolio might get ballast, and which managers are being paid to do more than ride the tape.

For advisors, that means the discussion around long short equity hedge funds has to be practical. The strategy shouldn't be introduced as a mystery box or an institutional badge of sophistication. It should be framed around a simple issue: can this allocation provide a return stream that behaves differently enough to earn its seat?

Practical rule: If a strategy is sold as a hedge, the evaluation has to focus on what it actually hedges, when it hedges, and what clients give up in exchange.

The role these funds can play

The appeal is understandable. A manager can buy stocks expected to rise and short stocks expected to fall. That setup sounds like a cleaner way to monetize security selection while muting broad market risk. In the right hands, it can be.

But the key phrase is in the right hands. Some long short equity hedge funds are disciplined tools for lowering directional exposure and seeking stock-specific alpha. Others merely carry enough net market exposure that they behave more like expensive equity funds when stress hits.

That distinction matters because advisors aren't allocating to a concept. They're allocating to an implementation. Liquidity terms, structure, net exposure discipline, short book construction, and communication standards all affect the result clients experience.

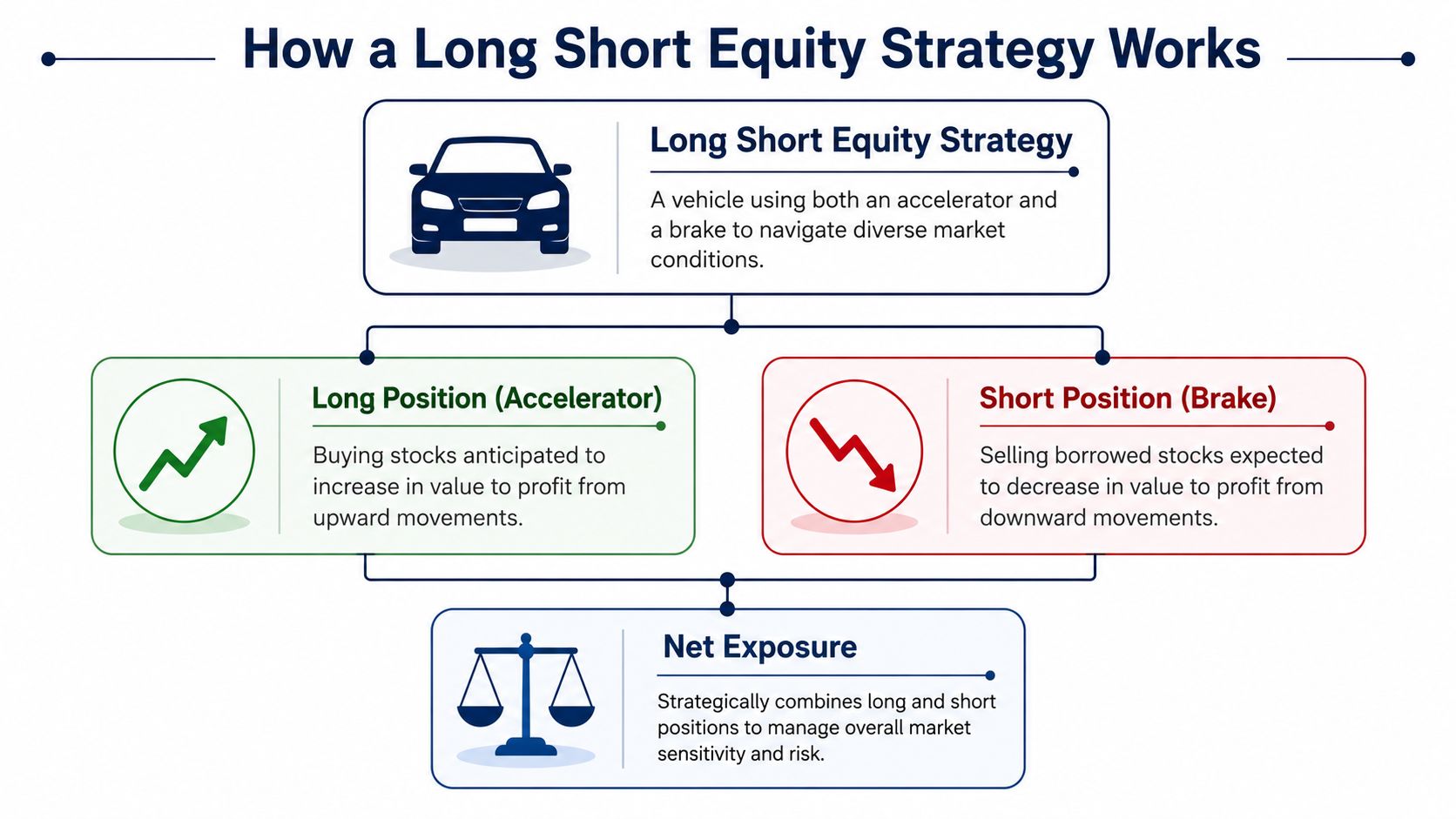

How a Long Short Equity Strategy Works

The cleanest way to explain the mechanics is with a car. The long book is the accelerator. The manager buys securities believed to be undervalued and expected to appreciate. The short book is the brake. The manager borrows shares through a brokerage, sells them, and aims to repurchase them later at a lower price.

A traditional long-only portfolio mostly drives with the accelerator pressed. A long short equity strategy can speed up, slow down, or stay nearly balanced depending on the manager's design. That flexibility is what makes the strategy useful and what makes manager evaluation essential.

The engine behind the strategy

A sound description starts with exposures.

- Long exposure means the capital committed to stocks expected to rise.

- Short exposure means the capital committed to positions expected to decline.

- Gross exposure is the total of long and short exposure. It reflects how much overall risk the portfolio is taking on through both sides of the book.

- Net exposure is the long exposure minus the short exposure. It tells advisors how much directional market risk remains after the short book offsets the long book.

According to Morgan Stanley's discussion of long short equity strategies, long short equity funds generate returns by converting individual stock selection views into an efficient return source while explicitly reducing market beta. Managers typically maintain at least 50% exposure to equities through long and short positions, while curtailing net exposure to a narrower band such as market-neutral at -10% to 10%, low net at 10–30%, or mid or variable net at 30–60% to mitigate volatility and drawdowns versus long-only counterparts.

That's the strategic core. The manager isn't trying to be right only about whether equities in general will rise. The manager is trying to be right about which stocks should outperform which other stocks, while controlling how much market direction influences the result.

Net exposure drives behavior

This is the part clients rarely hear explained clearly.

A fund with a low or near-zero net exposure is built to keep broad market movements from dominating outcomes. A fund with a higher net exposure is still directional. It may have a short book, but it can still participate meaningfully in market drawdowns because the long side remains larger than the short side.

That distinction changes client expectations.

| Exposure concept | What it means in practice |

|---|---|

| High gross exposure | The manager is expressing many views, often with leverage or a larger total position set |

| Low net exposure | The fund is trying to reduce market sensitivity and rely more on selection skill |

| Higher net exposure | The fund retains more equity-like behavior, with the short book acting as a partial offset |

A short book is not automatically a hedge. It's only a hedge if its size, construction, and timing materially offset what the long book loses when markets fall.

The skill set behind successful long short equity hedge funds is demanding. Fundamental managers often rely on financial statement work, earnings analysis, management meetings, and supply chain scrutiny. Some managers add quantitative tools, but the same principle holds. The strategy works when the manager identifies mispriced securities on both sides and manages risks that can damage returns, including short squeezes and borrowing-related volatility.

For advisors, the takeaway is simple. The presence of shorts doesn't make a fund defensive by default. Net exposure, short book quality, and risk controls determine whether the brake slows the car.

Analyzing Return Risk and Fee Structures

Clients often assume long short equity hedge funds should outperform in every market. That's the wrong benchmark. A well-run strategy often looks most useful over a full cycle, not during a one-way sprint higher in equities.

What clients should expect

The better expectation is different behavior, not constant outperformance. These strategies are usually designed to lower sensitivity to broad market swings, dampen drawdowns, and create room for manager skill to matter more than market direction.

A common portfolio construction pattern reflects that goal. According to Repool's overview of long short equity allocation, portfolio allocation is typically balanced, with 40-60% of capital deployed in long stock positions and 40-60% in short positions to neutralize overall market exposure and reduce directional sensitivity.

That doesn't mean the ride is smooth. Short books can hurt during sharp rallies. Long books can lag in highly speculative tapes. Managers can also be right on the thesis and wrong on the timing. The return path can be frustrating, especially when clients compare it with a long-only benchmark during a strong bull phase.

A realistic performance framing

Advisors usually get better client outcomes when they describe the role this way:

- As a volatility management sleeve: It may help reduce dependence on market beta.

- As a stock-picking sleeve: It gives the manager a way to express positive and negative views.

- As a portfolio diversifier: It may behave differently from long-only equities, but that depends on implementation.

Fees can erase a good story

Fees deserve blunt treatment because they directly reduce net client outcomes.

The traditional private fund model is often described as 2 and 20, meaning a management fee plus a performance allocation. Structures vary, and the exact terms matter more than the nickname. Advisors need to review whether the incentive fee applies after losses are recovered, whether the fund uses a high-water mark, whether a hurdle exists, and how fund expenses sit on top of stated fees.

Client-safe framing: A manager can be skilled and still fail the allocation test if the fee load absorbs too much of the value created.

The practical question isn't whether a fee schedule sounds normal for alternatives. The question is whether the expected value after fees still justifies the complexity, liquidity profile, and diligence burden.

A clean due diligence conversation should ask:

- What return source is being purchased. Stock selection, market exposure management, or both.

- What friction is embedded. Management fees, incentive fees, trading costs, financing costs, and short-related expenses.

- What benchmark is fair. A low-net strategy shouldn't be judged the same way as a long-only growth fund.

When advisors skip this work, clients end up owning a complicated product with a simple problem. The net result doesn't justify the explanation required.

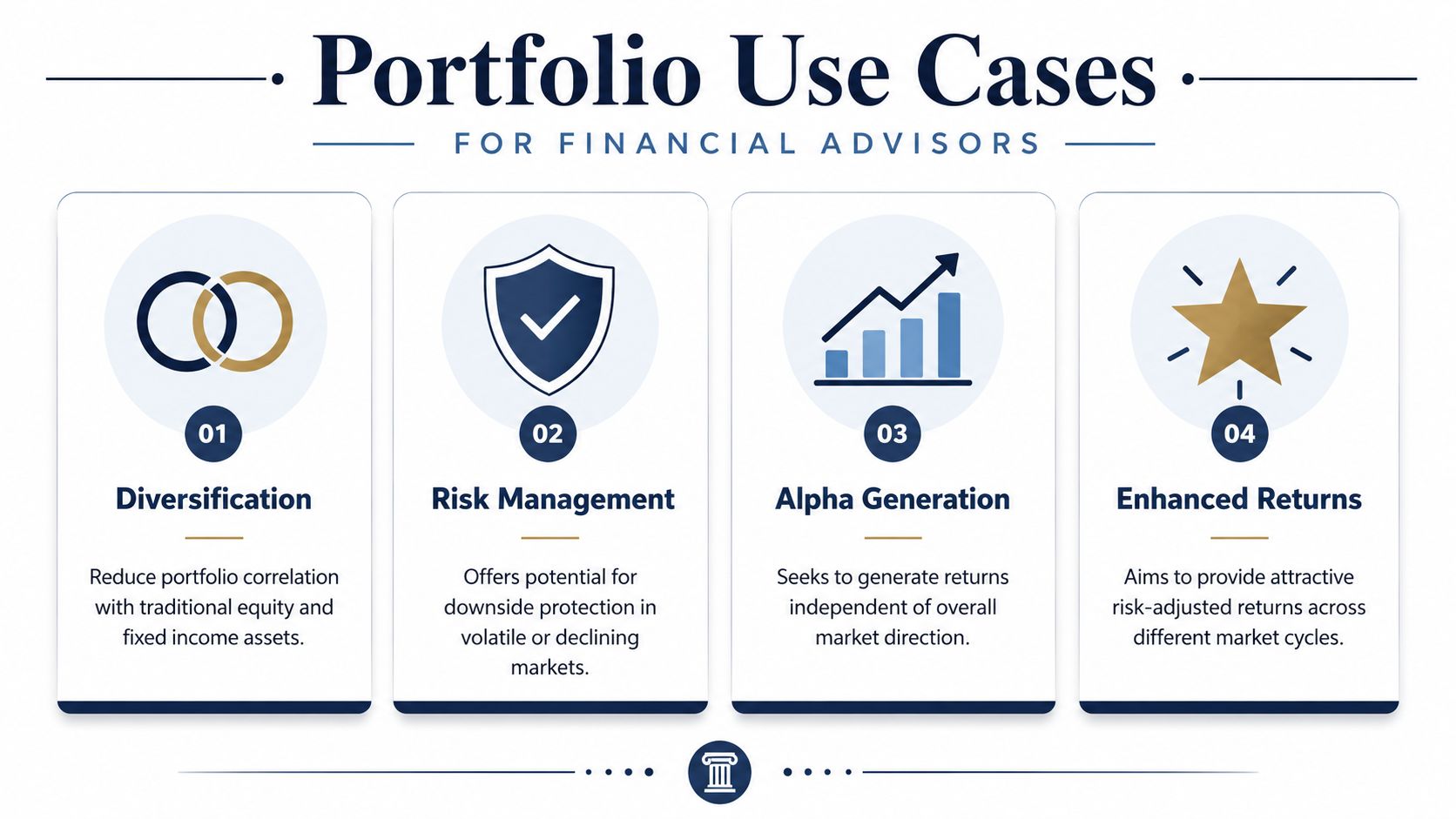

Portfolio Use Cases for Financial Advisors

Long short equity hedge funds earn their place when the advisor matches the strategy to a specific portfolio job. That job shouldn't be “own an alternative.” It should be tied to a concrete client objective such as lowering equity sensitivity, creating a differentiated source of return, or smoothing the path of a growth-oriented allocation.

Matching the strategy to the client objective

Not every long short mandate belongs in the same bucket. Mergers & Inquisitions explains that compared with long-only portfolios, long short strategies show lower sensitivity to market movements as measured by beta, volatility, and drawdowns. That same overview notes that directional Jonesian models allow 30–60% net exposure, while market-neutral models target net exposure around zero.

That creates a useful advisor framework.

For a client who wants a more defensive equity-related sleeve, a market-neutral implementation may fit as a complement to the growth allocation. The case isn't that it replaces bonds. The case is that it seeks return from relative stock outcomes rather than broad market direction.

For a client with higher risk tolerance who still wants to stay invested in equities, a variable-net or directional long short strategy can serve as a volatility dampener. The manager still carries directional exposure, but with a mechanism to offset part of the market's movement and exploit dislocations on both sides of the book.

Four common advisory applications

- Diversification within equities: Useful when the client already owns several long-only managers that behave similarly.

- Drawdown-aware growth portfolios: Helpful for clients who want equity upside participation but can tolerate less portfolio whiplash.

- Manager skill expression: Appropriate when the advisor has conviction that a manager can identify both winners and losers.

- Thematic implementation: Relevant when a manager specializes by sector or industry and can express relative views more precisely than a broad equity mandate allows.

Where advisors often get the fit wrong

The mismatch usually happens in client communication, not only in fund selection.

Some advisors present these funds as if every version is a hedge. Others place them in the alternatives bucket without defining the expected role. Clients then judge the position against the wrong standard. In strong markets they ask why it lagged. In weak markets they ask why it didn't protect more.

A better framing uses role-based language.

| Client need | Better long short fit |

|---|---|

| Lower market dependence | A lower-net or market-neutral structure |

| Growth with some shock absorption | A directional long short approach with controlled net exposure |

| Sector-specific inefficiency opportunity | A narrower strategy where manager expertise is central |

| Broader portfolio diversification | A strategy that complements, rather than duplicates, existing equity sleeves |

Advisors do best when they define success in advance. If the mandate is there to lower volatility, it shouldn't be defended later as a pure return-seeking strategy. If it's there to pursue alpha with some directional exposure, it shouldn't be sold as a crisis hedge.

A Due Diligence Checklist for Selecting Funds

Most allocation mistakes in this category begin with a headline assumption: if a fund is called a hedge fund and carries both longs and shorts, it must provide meaningful downside protection. That assumption doesn't hold up under scrutiny.

Start with skepticism, not the pitch deck

The most important reality check in this space is the hedging illusion. Data cited in this discussion of Greycourt's framing of equity long short correlation shows that in 2023, the average equity long short hedge fund had a 0.98 correlation with the broader market, meaning it moved almost in lockstep with equities and offered minimal hedge benefit during downturns.

That's not a small miss. It's a category-level warning.

A manager may still be worth owning with that kind of profile, but the fund should be accurately described. It may be an equity-like strategy with some flexibility, not a true diversifier. Advisors need that distinction because clients will remember the word “hedge” long after they forget the footnotes.

If a fund's correlation profile looks equity-like when markets are stressed, advisors should treat the hedge label as marketing language until the manager proves otherwise.

A working checklist for manager review

The cleanest due diligence process resembles vendor review more than product storytelling. The discipline used in practical guidance on vendor due diligence is useful here because both exercises require evidence, controls, and skepticism rather than trust in a polished presentation.

This checklist helps separate substance from branding.

Define the actual return engine

Determine whether the manager is primarily generating results from long book beta, short alpha, pair trading, sector rotation, or variable net exposure calls. A vague answer is a problem.Test downside behavior

Don't stop at full-period returns. Review how the fund behaved during market stress. The central question is simple: did the short book offset losses when it mattered?Inspect the short process

Shorting isn't just negative stock selection. Advisors should ask how the manager handles borrow availability, position sizing, squeezes, and timing risk.Separate alpha from market lift

If the fund's results rise and fall with the market, the advisor may be paying alternative fees for conventional exposure.Review operational fit

Redemption terms, gates, side pockets, transparency, valuation procedures, and reporting cadence all affect suitability.Assess organizational depth

Team stability matters. So does clarity around who owns idea generation, risk control, and trading execution. Firms that are growing this capability may also need the right hiring infrastructure, which makes specialized advisory staffing support relevant at the enterprise level.

Questions that belong in every manager call

- What did the short book contribute in a difficult market?

- How often does net exposure drift from stated targets?

- What risk limit forces a reduction in gross exposure?

- How concentrated can the short side become?

- What's the policy when a thesis is right but momentum moves violently the other way?

Due diligence lens: Advisors should underwrite process integrity first, portfolio behavior second, and performance claims last.

That order matters. Performance can impress for the wrong reason. Process failures eventually show up when liquidity tightens, prime broker conditions shift, or crowded shorts unwind quickly.

Marketing and Compliance in a Regulated World

Structure changes almost everything about how long short equity hedge funds are used, disclosed, and supervised. Advisors who skip that distinction create avoidable suitability and communication problems.

Structure changes the client experience

The first issue is access vehicle. According to CAIS on structural differences in long short equity offerings, hedge funds structured as limited partnerships have quarterly liquidity and high minimums, while ’40 Act funds and ETFs offer daily liquidity but operate with stricter diversification rules and position limits. Those constraints affect performance consistency and manager flexibility.

That means two funds with similar names can produce very different client experiences.

Long Short Fund Structure Comparison

| Attribute | Limited Partnership (LP) | '40 Act Mutual Fund | ETF |

|---|---|---|---|

| Liquidity | Quarterly liquidity | Daily liquidity | Daily liquidity |

| Investor access | Higher minimums, narrower investor base | Lower barriers to access | Lower barriers to access |

| Portfolio flexibility | Greater flexibility for manager implementation | Stricter diversification rules and position limits | Stricter diversification rules and position limits |

| Compliance posture | Heavier suitability and disclosure scrutiny | More standardized retail framework | More standardized retail framework |

| Client expectation risk | Often highest if terms aren't explained clearly | Lower if positioned accurately | Lower if positioned accurately |

An LP may suit a qualified client who understands limited liquidity, less standardized disclosure, and a more specialized mandate. A ’40 Act fund or ETF may fit better when the client values daily access, simpler custody integration, and a more familiar reporting framework.

How to talk about these funds without creating problems

Advisors and marketing teams should keep the communication standard simple. Describe the structure, the liquidity terms, the strategy's objective, the role in the portfolio, and the key risks in plain language. That includes short selling risk, amplification risk where applicable, and the possibility that the fund won't hedge effectively in all market conditions.

Marketing teams also need a process discipline that matches the product complexity. When firms build campaigns, webinars, landing pages, or advisor education around these strategies, the analytics should measure not just lead activity but also message quality, review friction, and conversion by audience type. Teams that want a better framework for evaluating reporting discipline can borrow ideas from MyMentions' analytics agency guide, especially around how to distinguish vanity metrics from decision-useful metrics.

A few practical rules help keep communications clean:

- Lead with function, not hype: Describe what the strategy seeks to do in a portfolio before discussing performance.

- Disclose structure-specific limits: LPs, mutual funds, and ETFs should never be discussed as interchangeable.

- Avoid blanket hedge language: If the strategy can remain meaningfully equity-sensitive, say so plainly.

- Align marketing with supervision: Content teams should work from approved language libraries and current disclosures, especially in digital campaigns and advisor-facing education.

- Match the channel to the complexity: A short social post can introduce the idea, but full risk explanation belongs in longer-form content and supervised conversations. Firms refining that process can learn from modern marketing systems for financial advisors, where compliant message architecture matters as much as promotion.

The compliance risk usually doesn't come from discussing a complex strategy. It comes from discussing it too casually.

That's especially true when advisors use shorthand such as “market neutral,” “downside protection,” or “alternative diversifier.” Each phrase creates an expectation. If portfolio behavior doesn't match the phrase, the communication issue becomes as important as the investment result.

Integrating Long Short Strategies Thoughtfully

Long short equity hedge funds deserve a place in the advisor toolkit, but only when the allocation decision is grounded in role clarity. These funds aren't broad solutions for every client concern. They're specialized instruments that can help when an advisor wants to reduce dependence on long-only equity beta, add a more flexible stock-selection sleeve, or introduce a strategy built to work on both the long and short side.

The discipline lies in resisting the label. A fund isn't useful because it sounds institutional or because it contains short exposure. It's useful when the structure fits the client, the manager's process is understandable, the fee load is justified, and the expected behavior has been explained in language the client can repeat back.

That makes the advisor's job straightforward, even if the strategy itself is not. Define the job first. Underwrite the manager second. Match the wrapper to the client third. Communicate the trade-offs with precision every step of the way.

Clients don't need every portfolio component to be exciting. They need each component to be intentional. In that sense, long short equity hedge funds are at their best when they're treated less like prestige products and more like carefully chosen tools.

Advisor Momentum helps financial advisors, RIAs, and banking teams turn complex topics into compliant, client-ready marketing. Firms that need stronger content, clearer brand positioning, or growth systems built for regulated environments can explore Advisor Momentum.