A lot of advisory firms are still running a surprisingly fragile planning process. One advisor has a strong discovery meeting but weak follow-through. Another builds detailed plans that stall after presentation. A third delivers good advice, yet every client relationship depends on memory, individual heroics, and back-office cleanup.

That pattern creates inconsistent client outcomes and operational drag. It also turns growth into a staffing problem. Each new household adds more exceptions, more rework, and more compliance exposure.

The firms that scale well usually treat the stages of financial planning as a business system, not a checklist. They standardize the sequence, define what must be documented at each point, and train the team to move clients from conversation to action without losing clarity or momentum.

Table of Contents

- Why Mastering the Financial Planning Process Is Non Negotiable

- Stage 1 Discovery and Defining the Relationship

- Stage 2 Gathering Comprehensive Client Data and Goals

- Stage 3 Analysis and Evaluating Financial Health

- Stage 4 Developing and Presenting the Financial Plan

- Stage 5 Implementing the Financial Recommendations

- Stage 6 Monitoring Progress and Adapting the Plan

Why Mastering the Financial Planning Process Is Non Negotiable

A formal process isn't bureaucracy. It's the operating model behind consistent advice, cleaner documentation, and better client retention.

The core framework is well established. The financial planning process is standardized into six key stages by the CFP Board and major industry bodies: establishing the client-planner relationship, gathering client data, analyzing information, developing recommendations, implementing the plan, and monitoring. That structure ensures advisors collect both quantitative and qualitative information before making recommendations, as outlined in this overview of the standardized financial planning stages.

When firms skip that discipline, they usually pay for it in three places. Advice gets less precise. Workflows become harder to delegate. Clients feel the difference between a conversation and a process.

For firms trying to scale, process design matters as much as technical planning skill. Resources focused on Support for financial professionals can help leadership teams think through how client communication, documentation, and operational support need to align around the planning workflow.

The Six Stages of Financial Planning At a Glance

| Stage | Core Objective | Primary Deliverable |

|---|---|---|

| Discovery | Define fit, expectations, and scope | Engagement terms and documented goals |

| Data Gathering | Build a complete fact base | Organized client data set |

| Analysis | Evaluate current financial position | Diagnostic findings and gap assessment |

| Plan Development | Translate analysis into advice | Prioritized financial plan |

| Implementation | Convert advice into action | Completed tasks and product execution |

| Monitoring | Keep the plan current | Review cadence and updated recommendations |

Practical rule: If a process can't be repeated by another team member without guesswork, it isn't a process yet.

The strongest firms don't treat the stages of financial planning as abstract doctrine. They use them to set service standards, define team handoffs, and create a client experience that feels both personal and dependable.

Stage 1 Discovery and Defining the Relationship

Discovery is where many firms either earn authority or accidentally weaken it. If this meeting feels vague, rushed, or overly product-focused, clients assume the rest of the relationship will feel the same way.

A strong first meeting does two jobs at once. It builds trust, and it defines the working relationship in terms clear enough for compliance, operations, and future service delivery.

Set the tone in the first meeting

The best discovery meetings follow an agenda. Not a rigid script, but a sequence that keeps the conversation human while ensuring the advisor collects the right information.

A practical flow looks like this:

Open with purpose

Explain how the meeting will work. Clients should know whether this is a fit conversation, a diagnostic discussion, or the start of a formal planning engagement.Surface goals before details

Early questions should focus on meaning, not math. Useful prompts include:- Lifestyle definition: “What does financial security look like in daily life?”

- Decision pressure: “What financial decision feels most urgent right now?”

- Trade-off awareness: “What are you willing to change, and what are you not willing to change?”

Identify constraints

Family obligations, business ownership, prior planning failures, concentrated positions, divorce history, and health concerns often shape the engagement more than asset totals do.Clarify expectations

The advisor should explain how planning, implementation, and ongoing review will work if the relationship moves forward.

Clients rarely object to process. They object to ambiguity.

What the engagement must define

The engagement letter isn't a formality. It's where scope creep gets prevented before it starts.

At minimum, the relationship should define:

- Scope of services that are and aren't included

- Compensation structure and how fees are charged

- Client responsibilities for providing information and making decisions

- Advisor responsibilities for analysis, recommendations, and follow-up

- Communication standards including meeting cadence and expected response times

- Third-party coordination when attorneys, accountants, or other professionals are involved

A weak discovery process often sounds polished in the room but produces poor internal clarity. Team members don't know what was promised. Clients assume broader coverage than the firm intended. Small misunderstandings become service problems later.

A good KPI here isn't just prospect-to-client conversion. It also includes the quality of goal documentation, the number of engagements that start with complete signed paperwork, and how often the team has to revisit basic scope questions after onboarding.

Stage 2 Gathering Comprehensive Client Data and Goals

Most planning mistakes begin as data mistakes. Not analytical mistakes. Not presentation mistakes. Missing facts, incomplete context, and soft assumptions.

This stage needs more than a checklist of statements. Advisors need a process that captures both the financial facts and the human context that shapes every recommendation.

Collect facts and context separately

The cleanest way to manage this stage is to split it into two categories.

Quantitative data includes income, assets, liabilities, tax documents, insurance coverage, cash reserves, retirement accounts, business interests, and estate documents. This is the foundation for a usable net worth statement and a realistic cash flow view.

Qualitative data includes goals, family dynamics, risk tolerance, upcoming life changes, philanthropic intent, decision style, and concerns the client hasn't yet tied to a numerical target.

Those two categories shouldn't be mixed into one generic questionnaire. When firms combine them badly, clients rush through both. The result is poor technical input and shallow emotional insight.

One issue advisors can no longer treat as niche is early-stage estate planning. Existing content often frames estate work as a pre-retirement topic, but 68% of millennials and Gen Z investors seek estate structures before age 35 to protect digital assets and side businesses, according to this discussion of early planning priorities. That means advisors need to ask about beneficiary designations, digital property, and ownership structures much earlier.

For firms building better intake systems, curated financial advisor resources can help teams tighten questionnaires, workflows, and onboarding documentation.

A workable data gathering checklist

A useful intake checklist should cover the following:

- Income sources including salary, variable compensation, business distributions, rental income, and irregular cash inflows

- Assets such as bank accounts, taxable accounts, retirement plans, real estate, ownership stakes, and reserve cash

- Liabilities including mortgages, lines of credit, tax obligations, student loans, and personal debt

- Protection planning with current insurance policies, coverage gaps, beneficiary choices, and ownership details

- Estate documents including wills, trusts, powers of attorney, and any outdated designations

- Modern asset categories like digital accounts, cryptocurrency holdings, online business revenue, intellectual property, and monetized side projects

- Behavioral factors such as previous market reactions, spending conflicts, and major planning anxieties

A simple client explanation works well here:

“The plan only gets as good as the facts behind it. If something is left out, the recommendation may look polished and still be wrong.”

What works is staged collection. Start with essentials, then request deeper records in batches. What doesn't work is sending a long portal list without context and hoping the client understands why every document matters.

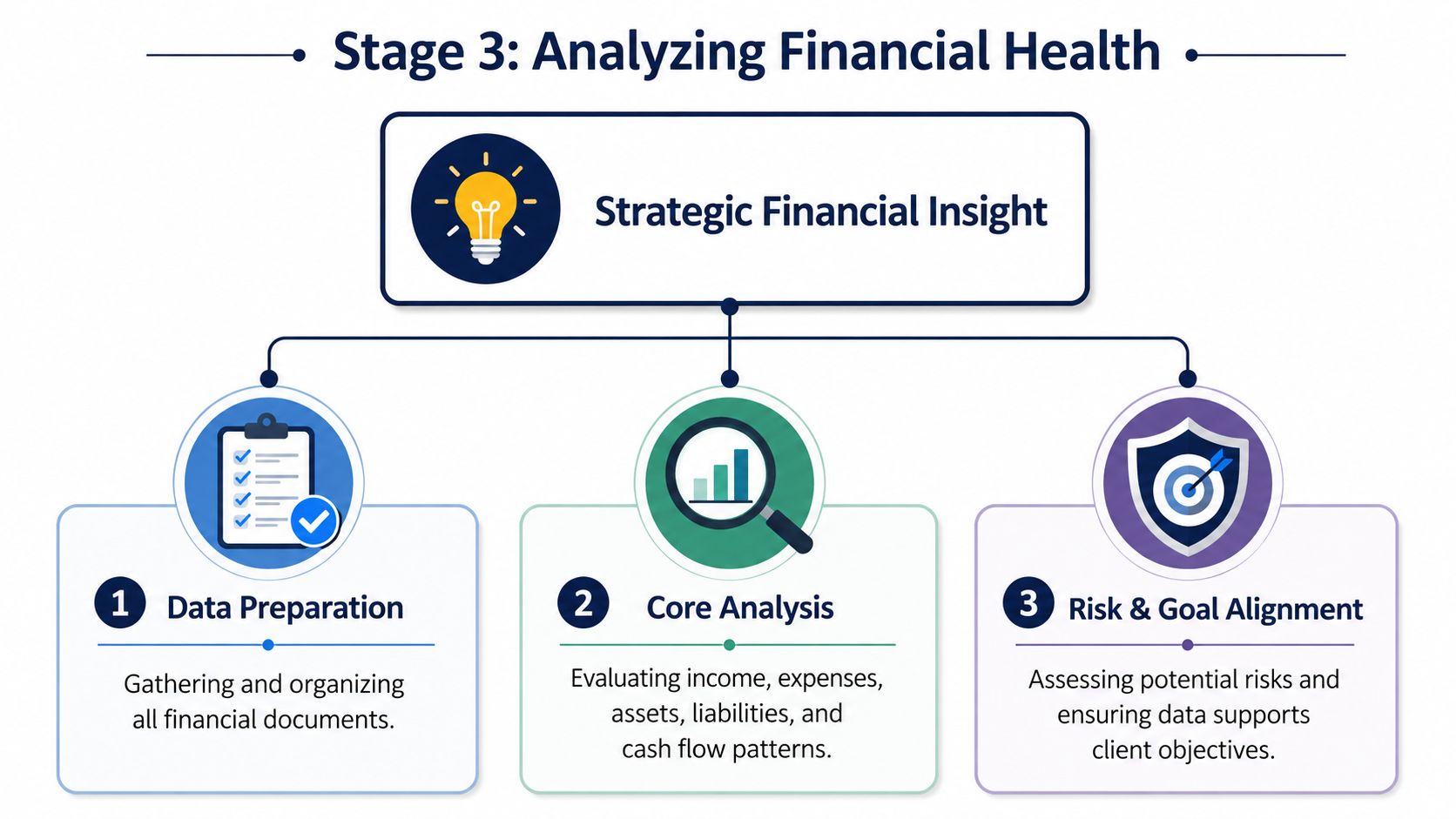

Stage 3 Analysis and Evaluating Financial Health

Analysis is where planning stops being administrative and starts becoming professional judgment. Clients don't hire advisors to collect PDFs. They hire them to interpret a financial life that often looks organized on paper and fragile underneath.

Weak analysis tends to do one of two things. It either produces a generic plan built around broad assumptions, or it jumps too quickly to solutions before establishing the client's current trajectory.

Start with the client's current reality

The CFP Board's updated process sharpened this point. Planners are required to analyze the client's current course of action and quantitatively calculate the probability of goal attainment. If that probability falls below a defined threshold, alternative courses of action must be identified, as explained in this review of the updated CFP planning framework.

That requirement matters operationally. It forces advisors to answer a foundational question before they recommend anything: what happens if the client changes nothing?

The analysis should usually begin with a small set of core outputs:

| Analytical Output | What It Reveals | Why It Matters |

|---|---|---|

| Net worth statement | Balance sheet strength | Shows liquidity, leverage, and concentration |

| Cash flow review | Spending and savings pattern | Identifies surplus, strain, and inefficiency |

| Goal probability analysis | Likelihood of reaching stated goals | Creates an evidence-based case for change |

| Risk exposure review | Protection and downside gaps | Connects planning to real-world vulnerability |

That sequence keeps planning grounded. It also helps the advisor separate urgent issues from important but less immediate ones.

What strong analysis actually produces

Good analysis doesn't dump data on the client. It produces decisions.

Examples include:

- A household with strong income and weak liquidity may need emergency reserves before aggressive investing.

- A business owner with healthy cash flow but outdated legal documents may need coordinated estate and protection work before tax optimization.

- A retired client with acceptable portfolio assets but unstable withdrawal assumptions may need spending adjustments and monitoring discipline before any allocation changes.

A common planning bottleneck sits inside risk evaluation. Advisors need a framework for discussing uncertainty in terms clients can act on. Broader reading on MakeAutomation's financial risk guide can be useful for firms thinking about how risk review, scenario planning, and operational workflows fit together.

The purpose of analysis isn't to prove expertise. It's to narrow choices intelligently.

Strong advisors also test the client's current habits, not just account values. Are savings happening consistently? Are liabilities being reduced intentionally? Are there estate documents that no longer reflect the family structure? Is insurance integrated into the broader plan, or sitting in a separate silo?

What works is documenting findings in plain language. “Current savings behavior doesn't support the retirement target” is clear. “Monte Carlo output suggests moderate insufficiency under stressed return assumptions” may be technically accurate but often fails to move the client.

A useful KPI in this stage is how often analysis leads to prioritized recommendations with clear rationale. If plans routinely emerge as long lists with no hierarchy, the analysis likely isn't sharp enough.

Stage 4 Developing and Presenting the Financial Plan

The plan document should reduce complexity, not showcase it. Many advisors still hand clients a technically sound report that no one wants to read and few feel ready to implement.

Clients need a plan they can follow. Teams need a plan they can execute. Compliance needs a record that shows how recommendations connect to facts and goals. One document has to serve all three purposes.

Build the plan in a client friendly order

A modern plan works best when it moves from high-level priorities into specific recommendations. That usually means starting with findings, then sequencing action items by urgency and dependency.

A practical structure looks like this:

Client priorities summary

Restate the goals in the client's language. This keeps the plan anchored to what matters most.Current position snapshot

Show the major findings from analysis. Keep this concise and visual.Key planning gaps

Identify where current behavior, structure, or documents fall short.Recommended actions

Present actions in order, usually immediate, near-term, and ongoing.Implementation map

Specify what gets done, by whom, and in what sequence.Review triggers

Note the life events or financial milestones that should prompt re-evaluation.

When budgeting guidance belongs in the plan, simplicity wins. The 50/30/20 rule remains a useful framework, allocating 50% to needs, 30% to wants, and 20% to savings and investments, as described in this financial planning guide from U.S. Bank. Advisors don't need to force every client into that formula, but it can make spending trade-offs easier to explain.

How to present recommendations so clients act

Presentation is not a recital of the plan. It's a decision meeting.

That means each recommendation should be tied directly to a stated goal, a diagnosed gap, or a risk that needs attention. The conversation gets stronger when the advisor links action to outcome in plain English.

Useful language includes:

- Goal connection: “This recommendation supports the retirement income target because the current savings path doesn't.”

- Priority framing: “This comes first because other recommendations depend on having liquidity in place.”

- Trade-off framing: “If this change feels too aggressive, there are slower alternatives, but they require accepting a different timeline or outcome.”

“The plan isn't asking the client to do everything at once. It's asking them to do the right things in the right order.”

Visuals help here. A one-page priority sheet, a timeline, or a short implementation roadmap can outperform a long appendix of assumptions.

Handling objections without losing momentum

Objections are rarely about the technical recommendation alone. They usually come from uncertainty, fear of change, or confusion about sequencing.

Three responses work better than overexplaining:

- Slow the pace when the client feels overwhelmed. Break recommendations into phases.

- Clarify the consequence of delay without sounding punitive.

- Offer a decision path instead of demanding immediate agreement on every point.

What doesn't work is treating the presentation as a one-way download. Advisors who talk for most of the meeting often leave with verbal agreement and weak follow-through.

A solid KPI for this stage is the percentage of plans that end with documented client decisions, not just “good meeting” notes. Another is the share of recommendations accepted with a clearly assigned next step.

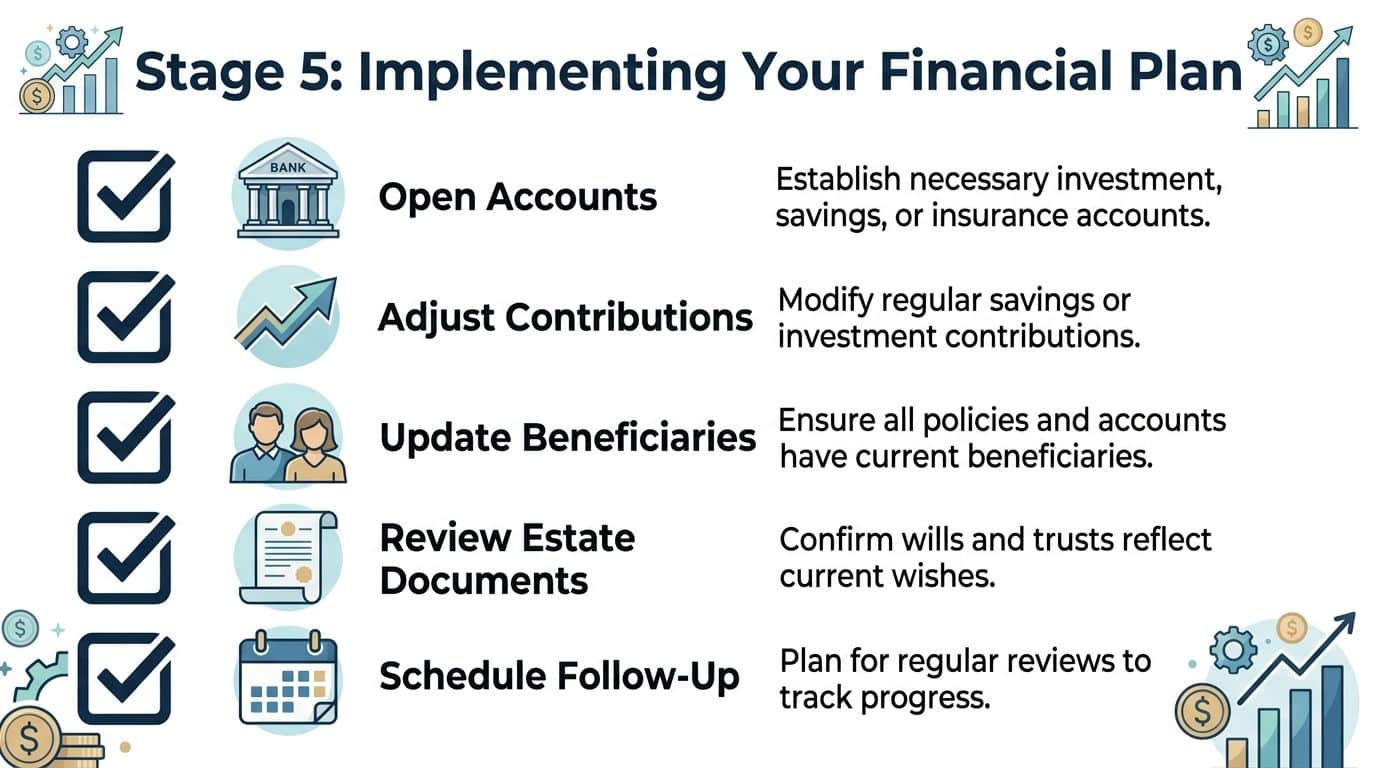

Stage 5 Implementing the Financial Recommendations

At this stage, many planning firms lose the value they worked hard to create. The recommendation is sound. The client is agreeable. Then nothing happens for weeks.

Implementation is the most operational stage in the stages of financial planning. It requires project management, clear ownership, and enough structure to move clients from intention to completion.

Why implementation is where value is created

The planning gap is real. Client adherence rates improve by approximately 30% to 40% when the advisor's scope explicitly includes implementation support and monitoring, according to the CFP Board guide to the planning process. That tells advisors something important. Clients often don't need more recommendations. They need more guided execution.

The core issue is responsibility. If no one owns each action item, the plan becomes a stack of good intentions.

Implementation should answer five questions for every recommendation:

| Question | Example of a Clear Answer |

|---|---|

| What is the action? | Increase retirement contribution or update beneficiaries |

| Why now? | It addresses the highest-priority gap |

| Who owns it? | Client, advisor, or outside professional |

| What is needed? | Forms, signatures, policy review, account opening |

| When is it due? | Target date with follow-up scheduled |

For firms under growth pressure, execution bottlenecks often expose staffing problems before anything else. If advisors spend too much time chasing paperwork and coordinating task completion, the service model starts to stall. Teams reviewing operational capacity often benefit from examining staffing support for advisory firms as part of the broader planning workflow.

A practical implementation workflow

A workable implementation meeting should end with documented tasks, owners, and dates. Not broad enthusiasm.

That workflow often includes:

- Account actions such as opening, transferring, retitling, or consolidating accounts

- Contribution changes tied to savings or debt strategy

- Protection updates including policy review and beneficiary adjustments

- Estate coordination to confirm wills, trusts, and powers of attorney align with the plan

- Follow-up scheduling before the meeting ends

One area where specificity matters is emergency reserves. Fidelity recommends a two-phase approach: first save $1,000 or one month of essential expenses as an immediate buffer, then build the fund to cover 3 to 6 months of essential expenses in a safe, accessible vehicle, while keeping $1,000 readily available at all times, as described in Fidelity's planning steps for emergency savings.

That kind of recommendation works because it feels achievable. “Build a full reserve” can sound abstract. “First secure the initial buffer, then complete the full target” gives the client an actionable path.

Execution standard: Every recommendation should leave the meeting with an owner, a due date, and a documented next touchpoint.

What doesn't work is vague implementation language like “client to consider,” “advisor to follow up,” or “estate work recommended.” Those notes create false completion. The recommendation exists on paper, but nobody can tell whether it moved.

Strong KPIs here include implementation completion rate, time from plan approval to first completed action, and the share of recommendations that remain stalled without documented intervention.

Stage 6 Monitoring Progress and Adapting the Plan

A financial plan isn't finished when the signatures are done. It stays valid only as long as the client's life, cash flow, assets, and priorities remain close to the assumptions behind it.

Monitoring needs structure. Annual reviews are the minimum baseline, but the better model is a recurring agenda that combines plan progress with life-change detection.

Turn reviews into a system

A clean review agenda usually covers:

- Progress against goals and whether the client is still on the intended path

- Changes in balance sheet or cash flow that affect the original recommendations

- Implementation status on any unfinished action items

- Document review for beneficiaries, insurance, and estate items

- Forward-looking changes such as retirement timing, business transitions, caregiving, or relocation

The team should also track internal service KPIs. Client retention, review completion cadence, open planning tasks, and updated documentation rates all show whether monitoring is active or merely promised.

Prepare for non linear life events

The biggest weakness in many service models is assuming financial progress is linear. It isn't.

Only 12% of high-net-worth clients have a formal protocol for emergency re-planning after a major life shock, according to this discussion of non-linear financial planning needs. That's a major opening for firms willing to build adaptive review protocols around divorce, job loss, health events, inheritances, and sudden business changes.

The practical fix is simple. Define triggers that move a client out of the normal review cycle and into a re-planning workflow. That might include immediate cash flow review, revised priorities, updated risk analysis, and a short-term action plan.

A firm that monitors well doesn't just preserve the plan. It reinforces its value every time life changes.

Advisor Momentum helps financial advisors, wealth managers, and banking teams turn good planning processes into scalable growth systems. From compliance-ready content and websites to coaching, branding, and recruiting support, Advisor Momentum is built for regulated firms that want sharper client experiences and stronger operational execution.