A familiar pattern is playing out across advisory firms and banking teams. Referrals still come in, seminars still happen, and long-standing client relationships still matter. But the pipeline feels less predictable because prospects now vet firms online long before they return a call, fill out a form, or ask for a meeting.

That shift exposes a hard truth. Many firms still look interchangeable on the web. Their websites say the same things, their social posts sound generic, and their marketing either gets slowed by compliance at the last minute or goes live without a measurement model that can prove what worked. In regulated markets, digital visibility alone isn't enough. A firm needs visible expertise, operational discipline, and a way to connect education to eventual revenue.

That is what makes digital marketing in financial services different from standard channel advice. The work is less about chasing whatever tactic is popular this quarter and more about building a compliant system that earns trust, survives review, and supports a long buying cycle.

Table of Contents

- The New Reality for Financial Marketing

- Navigating the Compliance Tightrope

- Building Your Digital Foundation

- Compliant Strategies for Key Digital Channels

- Measuring Real ROI in a Long Sales Cycle

- Your Implementation Roadmap and Team

- What Compliant Execution Looks Like

- Your Partner in Compliant Growth

The New Reality for Financial Marketing

A prospect gets a recommendation for a financial advisor, searches the firm name on a phone between meetings, opens the website, scans a dated homepage and a thin bio, then leaves. The referral was strong. The digital follow-through was weak.

That pattern shows up across advisory firms, banks, and credit unions. Good service and solid products do not carry as far as they used to if the online experience creates doubt, slows the next step, or feels interchangeable with every other institution in the category.

The crowded digital shelf

Financial firms now compete for attention in one of the most expensive digital categories. Research cited by The New York Times Licensing Group notes that financial services account for more than 14% of online ad spend, and mobile banking use among younger consumers is now mainstream, which raises the standard for speed, clarity, and usability in every digital touchpoint, as outlined in its financial content marketing data roundup. For marketers inside regulated firms, that means a weak website is not a branding issue alone. It is a revenue issue.

The firms that win online usually answer a few questions fast:

- Who is this for? Broad messaging attracts traffic but often lowers conversion quality.

- Why trust this team? Clear credentials, a defined process, and current educational content do more than polished slogans.

- What should I do next? Prospects need a direct path to book a meeting, start an application, or ask a specific question.

- Is this business active and current? Stale insights, outdated rates, and neglected profiles create avoidable doubt.

I see the same mistake repeatedly. Teams publish content, run ads, or refresh social channels before they fix positioning, proof, and conversion paths. That creates activity without much progress.

The better approach is controlled differentiation. Firms need messaging that reflects their actual strengths, then they need review workflows that keep that messaging compliant across channels. Teams testing newer formats can study broader AI and video marketing tactics, but financial marketers still have to translate those ideas into approved language, documented disclosures, and retained records before anything goes live.

Visibility alone isn't the goal

More traffic does not solve much if the wrong visitors arrive, or if qualified prospects cannot tell what makes the firm credible. In financial services, digital marketing has to support a longer trust cycle. A prospective client may first find a blog post, return later through branded search, read emails for weeks, and convert only after a referral or life event creates urgency.

That is why this work should be judged on pipeline quality and progression, not surface metrics alone. A fundamental shift in financial marketing is not merely becoming more digital. It is building digital systems that can earn trust, pass review, and produce measurable business outcomes over time.

Navigating the Compliance Tightrope

Compliance anxiety stops more campaigns than poor creative. A marketing team drafts a useful article or a sharp landing page, then review begins late, edits pile up, and launch slips. The deeper problem isn't caution. It's sequencing. When compliance enters at the end, it acts like a brake. When it enters at the start, it becomes part of the build.

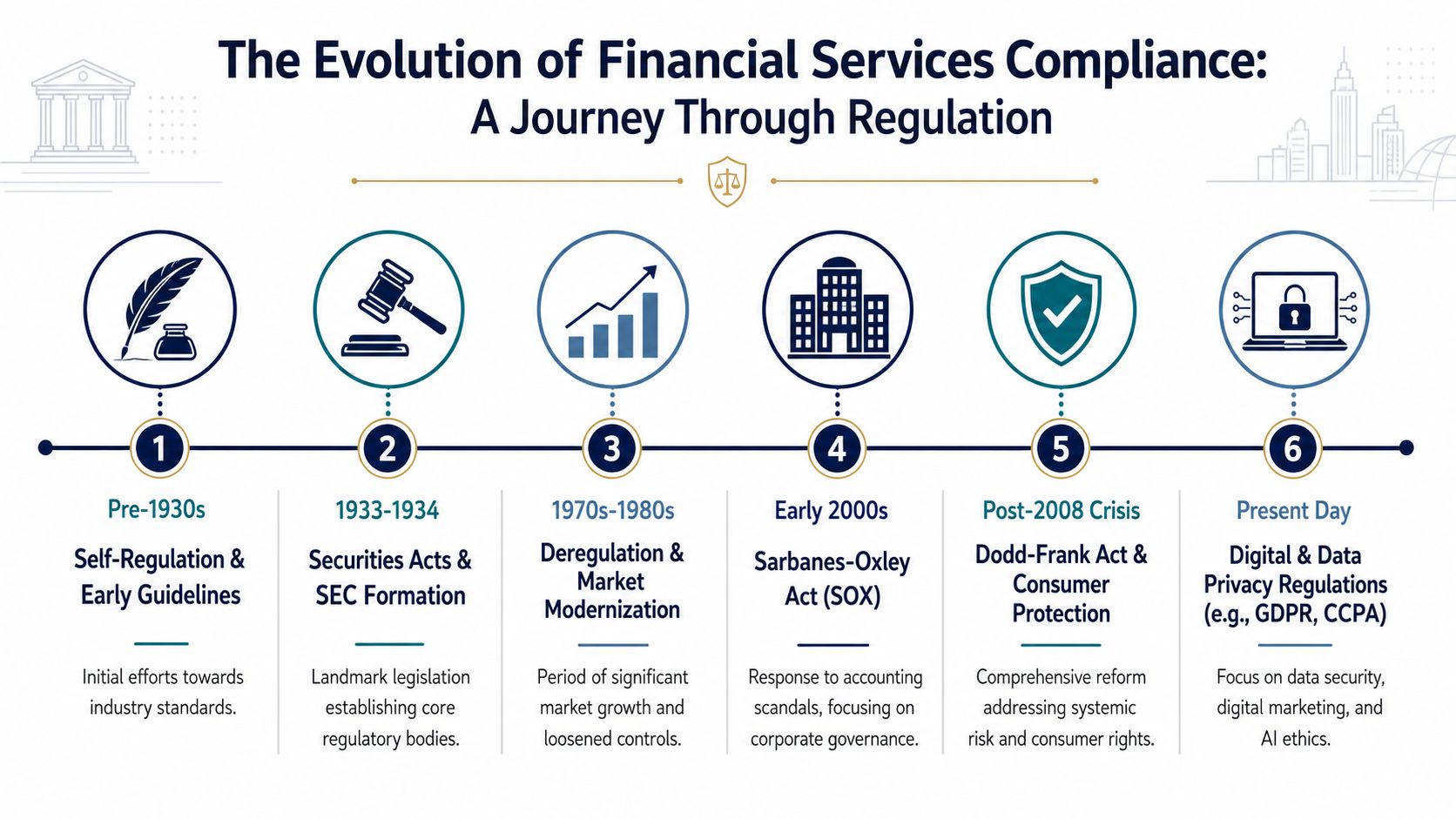

Why the rule changed day-to-day marketing

For advisers, the practical baseline changed when the SEC Marketing Rule did. The rule, formally Rule 206(4)-1, went into effect on May 4, 2021, with a mandatory compliance deadline of November 4, 2022, and it expanded the definition of advertisement to include virtually all digital communications made to more than one person, including websites, social media, and email campaigns, as outlined in this SEC marketing rule compliance guide.

That matters because many firms still behave as if only formal ads require formal controls. In practice, routine digital content can trigger review concerns if the firm hasn't documented standards for what can be said, how claims are substantiated, and where records are stored.

A simple operating model helps:

Define content categories early

Educational articles, promotional landing pages, event invitations, newsletters, and social posts don't carry the same level of risk. Review rules should reflect that.Set approval paths by risk level

Not every asset needs the same escalation route. But every asset needs a documented route.Write with substantiation in hand

If a statement can't be supported, it shouldn't ship. That applies to service claims, outcome language, and performance references.Archive what was published

Final approved versions, dates, disclosures, and related review notes should be retained consistently.

What compliance-first execution looks like

A compliance-first program doesn't read like legal copy. It reads clearly, avoids implied guarantees, and makes disclosures part of the experience instead of an afterthought. Firms that operate this way usually standardize the basics across channels.

A practical checklist looks like this:

- Clear ownership: Marketing drafts, compliance reviews, and leadership approves according to written policy.

- Disclosure placement: Required language appears where a reasonable reader will see it, not hidden below the fold.

- Privacy alignment: Data capture forms, cookies, and retargeting plans align with documented privacy standards.

- Testimonial controls: Social proof, endorsements, and reviews are handled under explicit written guidance.

- Human review: Drafting assistance can speed production, but a qualified reviewer still has to evaluate final content.

Compliance also extends beyond securities-specific issues. Firms need explicit policies for content creation, review, and approval workflows to reduce legal and reputational risk under regulations such as GDPR, CCPA, and FINRA, as discussed in this overview of digital marketing for financial services.

Practical rule: If the team can't explain why a statement is fair, balanced, and supportable, that statement isn't ready for publication.

A compliant marketing program doesn't avoid persuasion. It avoids ambiguity. The most effective firms understand that clarity itself is persuasive because it signals professionalism, controls risk, and lowers friction for prospects who are already cautious.

Building Your Digital Foundation

Firms often want more leads when what they need first is a better destination. Paid traffic, search traffic, referral traffic, and email traffic all fail in the same way when the website is confusing, generic, or operationally disconnected from intake.

A website has to do more than look polished

A financial services website has three jobs. It has to establish trust, explain relevance, and move the right visitor toward a compliant next step. If any one of those breaks, the site becomes a brochure instead of a growth asset.

That means the homepage can't carry the entire burden. Service pages need to speak to specific needs. Bio pages need to do more than list credentials. Contact paths need to reflect how the firm accepts inquiries. Educational content needs to connect to a nurture path instead of ending at a dead page.

The strongest foundation usually includes:

- A focused value proposition: It should explain who the firm serves and what problems it addresses.

- Visible trust markers: Professional standards, process explanations, and disclosure-ready language matter.

- Segmented pathways: Business owners, retirees, borrowers, and families don't all need the same journey.

- Integrated follow-up: Inquiry handling should connect to client relationship workflows, not sit in a generic inbox.

For firms reviewing how marketing handoff connects with service and retention, this look at client relationship management in financial services is useful because it highlights where lead generation often disconnects from the client experience.

Brand clarity reduces friction

Branding in regulated industries isn't decoration. It is decision support. A clear brand helps the market understand whether a firm is conservative, specialized, planning-led, community-focused, institution-backed, or designed for a narrow client profile. Without that clarity, all messaging becomes harder to trust because prospects can't tell what the firm stands for.

A quick comparison shows the difference:

| Weak foundation | Strong foundation |

|---|---|

| Broad language meant for everyone | Specific language aimed at a defined audience |

| Generic stock messaging | Point of view tied to real expertise |

| Contact form with no context | Clear next step and expectation setting |

| Compliance added at the end | Compliance built into templates and workflow |

Digital experience also now includes guided support. Many banking teams are evaluating conversational tools to handle basic questions, direct users to the right page, and reduce service bottlenecks. This review of Clepher's banking chatbot insights is a useful reference for how firms are thinking about chat-based interactions in a regulated environment.

A firm can outsource pieces of this work or handle them internally. One option in the market is Advisor Momentum, which provides website, branding, content, and marketing support built for advisory and banking teams. The more important point is structural, not vendor-specific. No campaign will outperform a weak foundation for long.

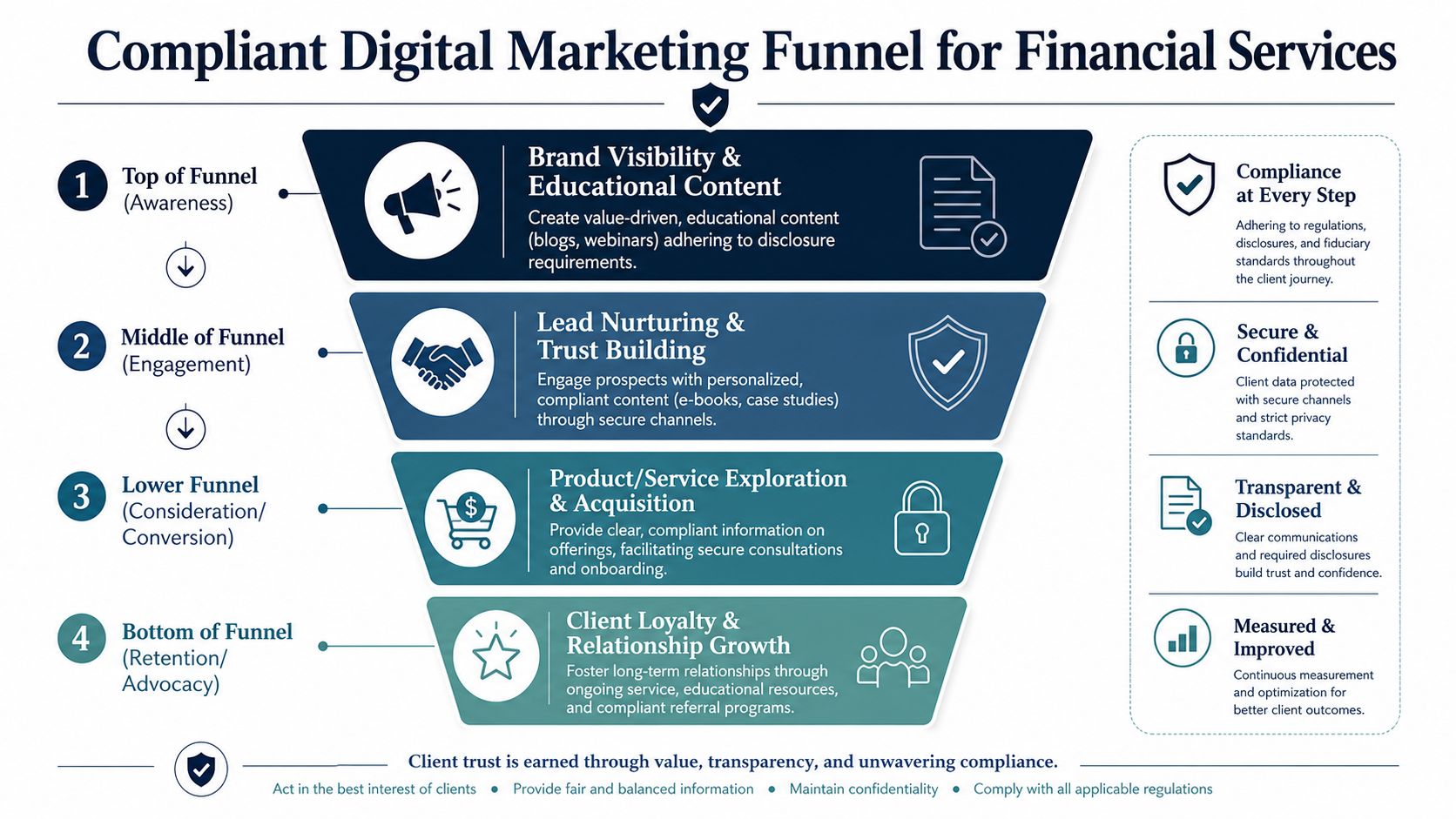

Compliant Strategies for Key Digital Channels

A prospect searches for a retirement advisor after a job change, clicks a paid ad, reads one article, watches a short video, then leaves. Three weeks later, that same prospect returns through a branded search and books a consultation. In financial services, that path is common. Channel strategy has to account for it, and compliance has to hold at every step.

Each channel needs a defined job. Search captures active demand. Content answers questions that stall action. Social supports credibility and familiarity. Paid media creates controlled visibility. Video helps prospects assess how a firm communicates before they ever speak to someone.

Search visibility with local intent and compliant copy

Search is often the cleanest demand signal available. People rarely search for financial services out of curiosity alone. They search because a planning issue, banking need, or lending decision is already in motion.

For regulated firms, the challenge is not just ranking. It is matching search intent with accurate, reviewable language. Local pages should reflect real offices, real service areas, and real differences in offer structure. Firms create avoidable risk when they publish thin location pages, use broad superlatives, or promise outcomes that the intake process cannot support.

A search program usually performs better when it follows a few operating rules:

- Build pages around decision-stage queries such as retirement rollover help, treasury management services, physician mortgage options, or fiduciary planning for business owners.

- Write titles and meta descriptions for clarity first so click-through gains do not come from language compliance would later have to pull back.

- Treat the business profile as part of the conversion path because many prospects decide whether to call from maps, reviews, hours, and category signals alone.

- Connect local visibility to branch or advisor operations so marketing is not driving inquiries into a poor handoff.

For firms that need stronger map pack visibility, this guide on improving your Google business listing for local search is a practical starting point.

Content that teaches without overpromising

Educational content works when it reduces confusion and sets up the next compliant action. It does not need to close the business on first touch. In fact, forcing a conversion too early usually lowers quality and creates a mismatch between what the visitor wanted and what the page asked them to do.

The highest-performing content programs in financial services usually share the same traits:

- Audience-specific topics tied to a defined client segment or account need

- Plain-language structure that explains trade-offs, timing, and terminology without sounding generic

- Clear disclaimers and scope limits when the topic could be read as individualized advice

- Next steps that match intent such as scheduling, downloading a checklist, subscribing to a topic series, or speaking with the right specialist

Weak content creates work for compliance and sales at the same time. It attracts the wrong audience, generates low-intent form fills, and leaves relationship managers correcting expectations that the marketing copy set poorly.

One test I use is simple. If a prospect finishes the piece, can they explain what the issue is, what factors matter, and what action comes next without assuming a guaranteed result? If not, the content is not ready.

Social media with supervision built in

Social should support trust, not chase relevance at any cost. Financial firms get better results from disciplined publishing than from reactive commentary.

A workable model usually includes three lanes:

Education

Short posts that explain common planning, banking, savings, lending, or fraud-prevention questions.Firm perspective

Updates on process, team expertise, community involvement, seminars, or service changes.Client retention support

Content that keeps existing relationships informed and engaged without drifting into personal recommendations.

Operational question is supervision. Who can post. What language is pre-approved. How comments are handled. Which content requires principal review. How records are archived. Firms that answer those questions before scaling social avoid the familiar cycle of aggressive posting followed by compliance pullback.

Paid search that qualifies instead of merely attracting clicks

Paid search can produce strong results in financial services, but it becomes expensive quickly because high-value categories attract aggressive bidding and careful consumers. Mobile expectations add pressure. Prospects expect the ad, landing page, disclosures, and form experience to work cleanly on a phone.

A 2024 banking benchmark from Insider Intelligence reported that mobile banking adoption among millennials in the United States was expected to reach very high saturation, with usage nearing universal levels among that group, according to Insider Intelligence's mobile banking forecast. That matters for campaign design. A paid click that lands on a slow page, a vague form, or a disclosure block that breaks on mobile is wasted budget.

The safer paid search approach is qualification first. Match keyword groups tightly to landing pages. Send early-stage traffic to educational assets. Reserve high-friction forms and appointment requests for prospects showing clearer intent.

This framework is useful:

| If the prospect intent is | Better destination |

|---|---|

| Early research | Educational article or guide |

| Comparing options | Service page with disclosures and process detail |

| Ready to act | Dedicated landing page with compliant intake step |

The trade-off is volume versus quality. Broad campaigns can create more leads on paper. Tighter campaigns usually create fewer, better conversations and less cleanup for advisors, bankers, and compliance reviewers.

Video that shortens the trust gap

Video helps prospects judge clarity, tone, and professionalism faster than text alone. That makes it useful in categories where trust is built over multiple interactions and where buyers want to understand the people behind the process.

The formats that usually hold up best under compliance review are repeatable and structured:

- One-question explainers that answer a single issue clearly

- Process walkthroughs that show what an introductory call, review meeting, or onboarding sequence includes

- Perspective videos that provide context on current conditions without drifting into personalized advice

- FAQ libraries that standardize answers to recurring questions

Governance decides whether video becomes an asset or a problem. Scripts, disclosures, speaker approvals, editing standards, and retention procedures should be set before production expands. Otherwise, firms scale inconsistency faster than they scale trust.

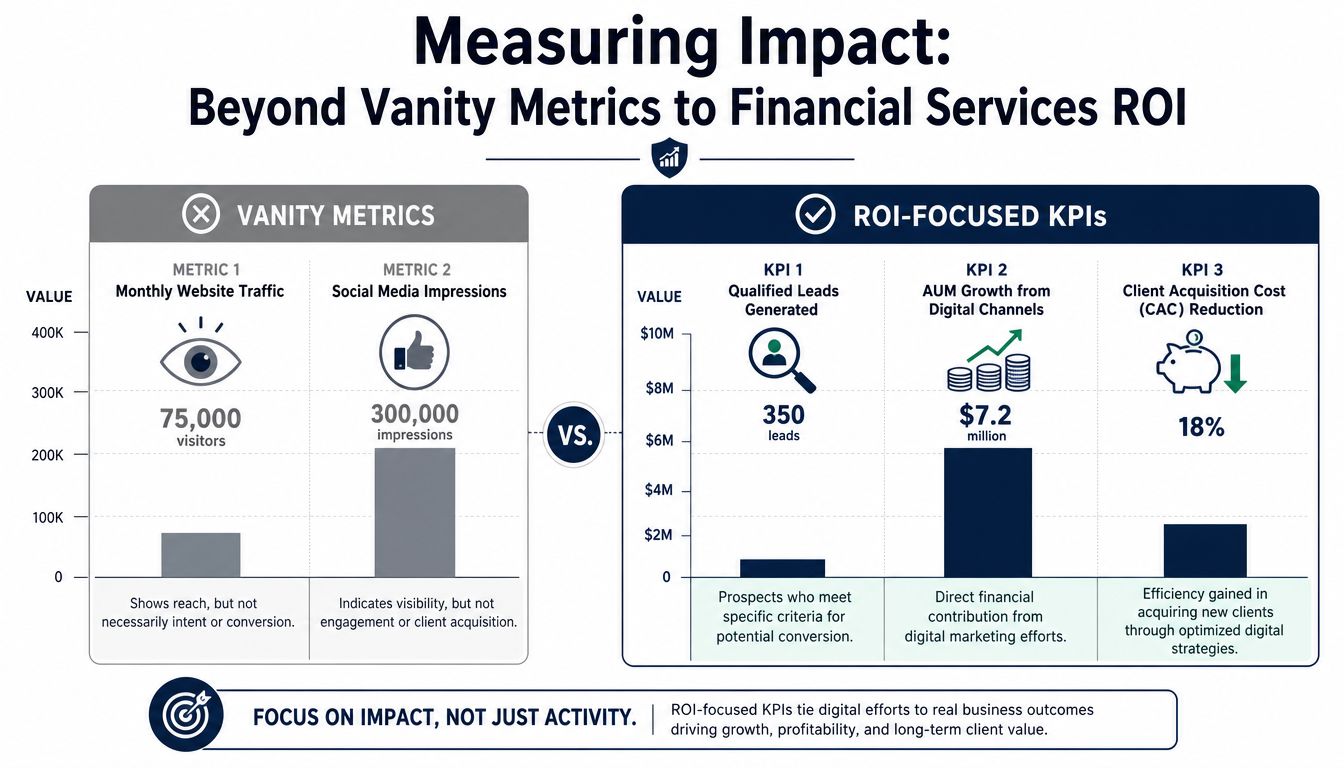

Measuring Real ROI in a Long Sales Cycle

Many financial firms still evaluate marketing as if the sale should happen within one session or one campaign. That model breaks quickly in advisory and banking environments because the buyer often spends time learning, comparing, discussing with family or colleagues, and revisiting the firm before taking action.

Why common KPIs fall short

Traffic, impressions, and engagement can show whether a message reached people. They don't show whether the right people moved closer to becoming clients. In long sales cycles, that distinction matters.

A recurring blind spot in the industry is educational content measurement. As Walker Sands notes, a common question is how financial advisors measure ROI for educational content, and the gap is the lack of attribution models that connect early-stage educational micro-moments to late-stage compliant onboarding, as described in this analysis of digital marketing for financial services.

That observation matches what many firms struggle with operationally. A prospect reads three articles, returns from search twice, attends a webinar, opens two emails, and only later books a meeting after a referral reminder. Last-click reporting gives nearly all credit to the final touch and almost none to the educational path that built confidence.

A better attribution model for advisory and banking teams

A more useful model tracks progression, not just conversion. Instead of asking which asset closed the sale, the better question is which sequence of interactions moved the prospect from anonymous interest to compliant onboarding.

The most useful ROI framework usually includes:

- Qualified inquiry definition: A form fill alone doesn't count if the prospect isn't a fit.

- Content engagement milestones: Repeat visits to service pages, educational content depth, and return sessions can indicate rising intent.

- Sales-stage mapping: Marketing should know when a prospect became an opportunity, not just when they entered the database.

- Time-to-onboard review: Long-cycle businesses need to understand how early content influenced the later sales window.

If a firm only measures the final click, it will underinvest in the content that made the final click possible.

A practical scorecard can look like this:

| Measurement area | Better question |

|---|---|

| Traffic | Which audience segment is returning with intent |

| Content | Which topics repeatedly appear before consultation requests |

| Lead quality | Which sources create qualified conversations |

| Revenue influence | Which campaign paths show up before onboarding |

This is also where email still matters. According to the Everfi summary of financial services marketing trends, the Data & Marketing Association reports that marketers earn about $35 for every dollar spent on email marketing, and the same source notes that 83% of U.S. digital banking users aren't hesitant about their providers using AI for marketing purposes while 40% of financial services professionals report lacking the tools needed for data-driven strategies, in this review of financial services marketing trends. The strategic point isn't that every firm should automate everything. It's that owned channels and personalization can support ROI when the measurement model is mature enough to connect nurture to conversion.

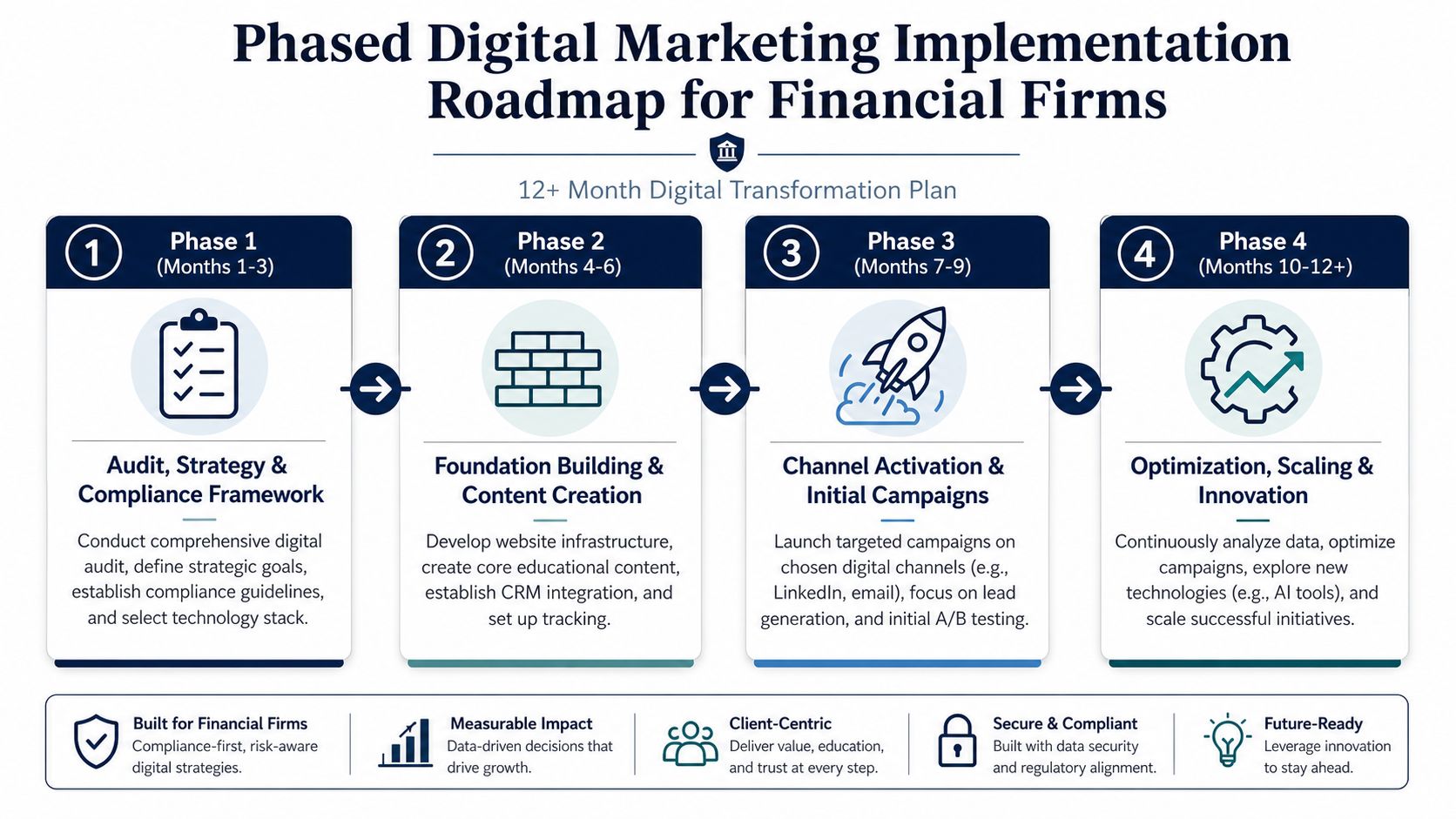

Your Implementation Roadmap and Team

Firms rarely fail because they lack ideas. They fail because execution gets spread across too many priorities at once. A workable roadmap sequences governance, foundation, production, and optimization in an order the firm can sustain.

Phase one starts with governance not campaigns

The first phase should feel less exciting than a launch plan because it is mostly audit work. That is exactly why it matters. Teams need a clear picture of current assets, review pathways, intake flow, tracking gaps, and message consistency before they add volume.

A four-phase roadmap usually works well:

Phase one

Audit the website, disclosures, forms, business listings, analytics, content library, and approval process. Establish content categories and review standards.Phase two

Rebuild or refine core pages, create foundational educational content, connect forms to the client intake path, and define reporting views.Phase three

Activate selected channels with tightly scoped campaigns. Start with a narrow audience, limited offers, and measurable handoffs.Phase four

Optimize with actual performance data, not assumptions. Expand only what the team can supervise consistently.

The team model that actually works

Digital marketing in financial services breaks down when no one owns the connective tissue between strategy, compliance, and operations. Marketing writes content. Compliance edits it. Operations receives leads. Sales follows up inconsistently. Reporting lives in separate places. Everyone is busy and no one has a full picture.

A stronger model gives each role a defined lane:

| Role | Core responsibility |

|---|---|

| Marketing lead | Strategy, calendar, channel management, reporting |

| Compliance reviewer | Policy alignment, disclosures, recordkeeping standards |

| Operations owner | Lead routing, intake process, follow-up workflow |

| Subject matter expert | Accuracy, relevance, topical perspective |

Real-time personalization is still a weak spot across the sector. Only 36% of large financial services firms personalize marketing programs based on real-time data, compared with 51% of technology companies, largely because outdated martech stacks prevent effective cross-channel personalization, according to The Financial Brand's reporting on future-ready marketing technology. That gap is why team structure and technology choices must be made together. An advanced strategy won't survive a fragmented stack.

The right stack doesn't need to be bloated. It needs to handle content workflow, approval visibility, lead capture, relationship tracking, reporting, and archive discipline. If the firm can't route a lead, see the content that influenced it, and verify what was approved, the stack isn't supporting the business.

What Compliant Execution Looks Like

Theory gets clearer when it turns into copy decisions. The difference between compliant and risky marketing usually isn't dramatic. It shows up in wording, placement, context, and process.

Example one independent RIA content

A weak LinkedIn post might say:

"Clients who followed this strategy came out ahead again. Reach out to see how to improve your returns."

That phrasing creates avoidable risk. It implies outcomes, lacks context, and sounds promotional without support.

A stronger version sounds like this:

"Recent market volatility has prompted many investors to revisit allocation, liquidity, and timeline assumptions. This article outlines questions households can review with their adviser when evaluating portfolio risk. It is provided for educational purposes and isn't individualized investment advice."

The same principle applies to blog disclaimers. A market trends article should clearly state that it is educational, that conditions can change, and that readers should evaluate decisions based on their own circumstances with appropriate professional guidance.

Example two retail bank campaign execution

A retail bank campaign often fails when the ad promises convenience but the landing experience creates friction. A stronger campaign aligns message and next step.

For example:

- Ad theme: Financial education around budgeting, fraud prevention, or account comparison

- Landing page: Simple explanation, disclosure-ready product detail, clear call to speak with a banker or start securely

- Follow-up: Nurture content tied to the topic the visitor viewed

Where performance enters the picture, precision matters even more. When investment advisers present performance results in advertisements, they must show net performance alongside gross performance with equal prominence and include returns for 1-, 5-, and 10-year periods, according to this summary of Rule 206(4)-1 advertising requirements. That means no oversized gross result in the headline with net figures buried in footnotes. Equal prominence means equal visibility in the actual presentation.

The safest compliant marketing rarely feels restrictive to the reader. It feels precise, balanced, and easier to trust.

A good internal test is simple. If a piece of marketing would confuse a prospect about what is factual, what is opinion, and what is conditional, it isn't ready.

Your Partner in Compliant Growth

Strong digital marketing in financial services isn't built on loopholes or trendy tactics. It is built on sound positioning, review discipline, measurable nurture paths, and execution that respects the buying cycle. Firms that treat compliance as part of strategy usually publish better content and convert demand more cleanly.

For teams evaluating outside support or broader planning frameworks, this guide to financial services marketing offers additional perspective on how specialized programs are structured. The lasting advantage, though, comes from choosing a partner that understands advisory and banking realities well enough to connect branding, lead generation, compliance, and operational follow-through.

Advisor Momentum helps financial advisors, RIAs, wealth managers, and banking teams build compliant digital growth systems that connect branding, websites, content, advertising, and coaching to real business outcomes. Firms that need a practical partner for compliant execution can explore Advisor Momentum to see how its financial-industry focus supports visibility, trust, and scalable lead generation.