A familiar pattern shows up in financial firms that are trying to grow. One advisor keeps client notes in a notebook. Another stores follow-up tasks in email folders. Operations has onboarding details in a spreadsheet. Compliance has archiving requirements in a separate system. When a prospect calls back after two weeks, the team knows the name but not the full context. When an examiner asks for communication records, staff starts piecing together a timeline by hand.

That setup doesn't just slow response time. It creates avoidable risk.

In financial services, client relationship management works best when it's treated as an operating system for the firm, not a digital address book. It should tell the team what happened, what needs to happen next, who owns the task, and what record must exist if a regulator asks for proof later. That's the fundamental shift behind modern CRM adoption. It moves relationship management from memory and individual habits into a repeatable business process.

That shift is happening across industries. The global Customer Relationship Management market reached $73.40 billion in 2024 and is projected to reach $163.16 billion by 2030, growing at a 14.6% CAGR. For financial firms, that growth matters because relationships are the business model. The firms that organize client data, service activity, and compliance records in one system can personalize at scale without losing control. The firms that don't usually feel the pain first in lead conversion, handoff errors, and exam preparation.

Table of Contents

- Introduction Beyond a Digital Rolodex

- The Core of Financial Services CRM

- Navigating Compliance and Data Governance

- Must Have CRM Features for Regulated Firms

- Selecting and Integrating Your CRM System

- Driving Adoption with Coaching and Change Management

- Measuring Success and Real World Examples

Introduction Beyond a Digital Rolodex

A CRM in financial services has to do more than store names, emails, and meeting dates. It has to connect prospecting, advice delivery, service, supervision, and recordkeeping in one controlled environment. If it doesn't, the firm ends up with a partial system that creates extra work instead of reducing it.

The practical definition is simple. Client relationship management financial services means building a structured way to capture client data, log interactions, manage workflows, and support compliant growth. Software matters, but strategy matters more. The system has to reflect how the firm acquires clients, onboards households, manages reviews, documents recommendations, and handles retention.

Why firms outgrow basic contact management

A basic contact database can hold names and phone numbers. That's not enough for a regulated business.

Financial firms need a record of what was discussed, when it was discussed, what documents were shared, what follow-up was promised, and which employee handled the interaction. They also need controlled access to sensitive information and retention practices that line up with supervision obligations. Without that structure, the team spends too much time searching for information and not enough time acting on it.

Practical rule: If an advisor can't open one record and understand the current relationship, the firm doesn't have a CRM strategy yet. It has scattered storage.

What a strategic CRM changes

When CRM is treated as a strategic system, three things improve at once:

- Lead handling gets sharper: New inquiries are routed, assigned, and followed up in a visible workflow instead of disappearing into individual inboxes.

- Service becomes more consistent: Review cadences, onboarding tasks, and client requests move through defined steps with clear ownership.

- Compliance gets easier to prove: The firm can show a documented process rather than relying on reconstructed explanations after the fact.

That's why the strongest CRM implementations in financial services usually begin with process mapping, not software shopping. The first question isn't which platform has the most features. The first question is where the current client journey breaks down, and what the system must enforce so those failures stop repeating.

The Core of Financial Services CRM

A good way to think about financial services CRM is as the firm's central nervous system. Information comes in from conversations, product activity, service requests, financial planning milestones, and internal tasks. The CRM collects that information, organizes it, and makes it usable by the right people at the right time.

Why the full client picture matters

A fragmented relationship creates fragmented service. An advisor may know the portfolio. A banker may know the lending relationship. A service associate may know the unresolved paperwork issue. If none of that sits in a unified record, the client experiences the firm as disconnected.

That problem matters because the relationship manager still carries the most trust. Research shows that 81% of banking clients identify their relationship manager as their preferred point of contact. Technology doesn't replace that role. It equips that role.

A proper 360-degree client record usually includes:

- Household and contact data: Key personal and account details needed for service and supervision.

- Communication history: Calls, emails, meetings, questions, commitments, and follow-up notes.

- Products and holdings context: What the client currently uses and what changed over time.

- Goals and risk profile: Planning priorities, suitability context, and major life updates.

- Open tasks and service issues: What's pending, who owns it, and when it's due.

What strong firms do differently

The strongest firms don't just collect more data. They collect the right data and make it actionable.

An advisor preparing for a review meeting shouldn't have to search across four systems for context. A service team member handling a beneficiary update shouldn't need to guess whether another department already spoke with the client. A business development lead shouldn't push a generic follow-up if the household is already deep in onboarding.

That's where workflow design matters. Firms that want better lead conversion often borrow discipline from broader nurturing frameworks, especially around handoff timing, message relevance, and follow-up ownership. A practical reference is this guide to B2B lead nurturing, which translates well when applied carefully to regulated advisory and banking environments.

For planning firms, the CRM should also line up with the actual client journey. The best systems mirror the progression from discovery through implementation and ongoing service, which is why many teams map workflows against the stages of financial planning rather than forcing every relationship into a generic sales pipeline.

The goal isn't more fields. The goal is fewer blind spots.

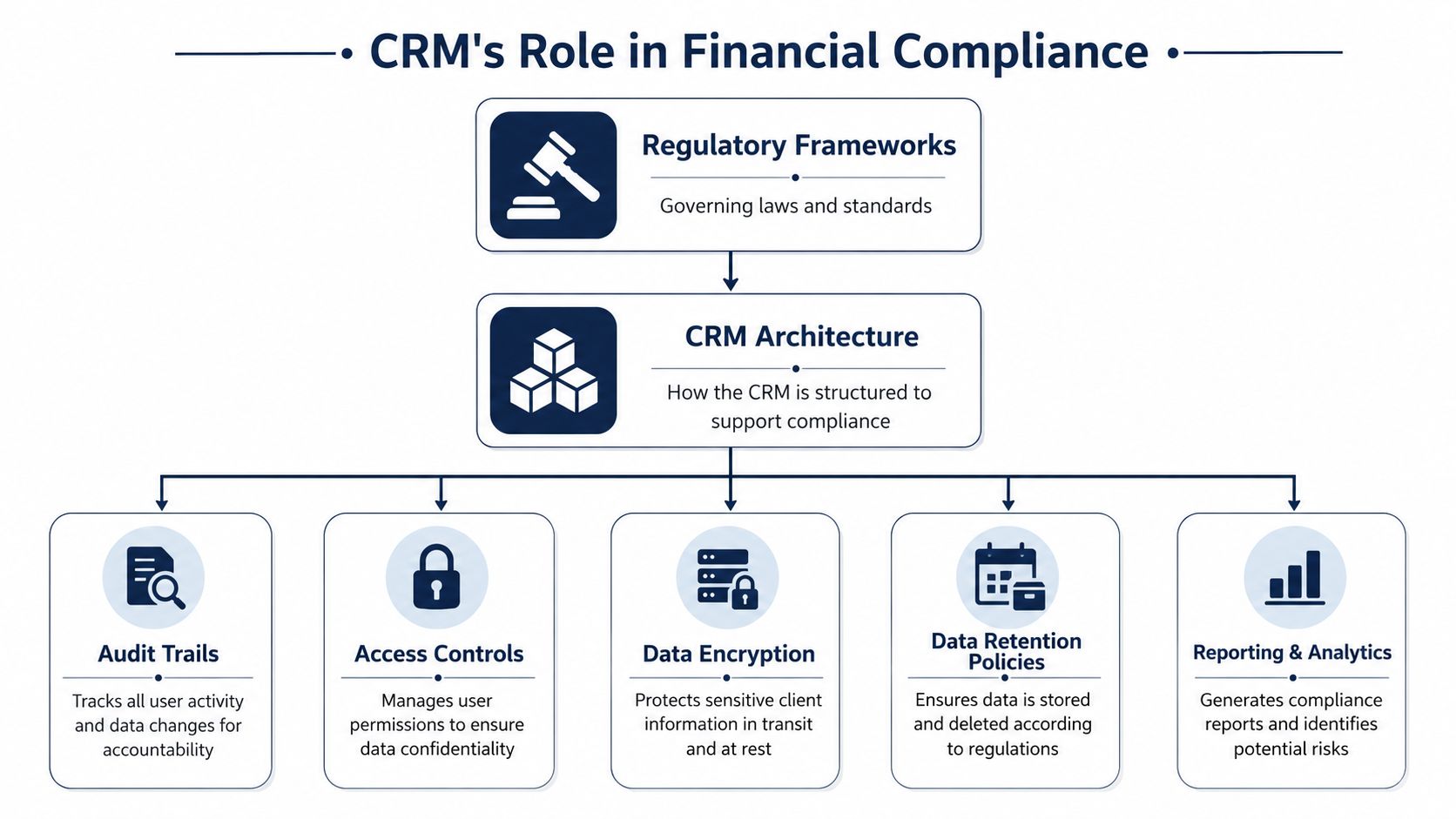

Navigating Compliance and Data Governance

In regulated firms, CRM architecture can't sit off to the side as a marketing convenience. It has to support supervision, record retention, controlled access, and defensible reporting. That's what turns a CRM into a risk management asset instead of a liability.

What regulators care about inside the workflow

Compliance pressure usually shows up in ordinary activity. A social post mentions results too aggressively. A website page changes and nobody archives the previous version. An advisor sends a personalized message that crosses into problematic performance language. A client complaint arrives by email and never gets tied back to the household record.

Centralization matters. Banking CRMs centralize client data to deliver a 360-degree view, enable audit-ready reporting, and use role-based access controls that mitigate compliance risk. That same source notes that banks using those features achieve higher audit compliance rates and faster generation of regulatory reports.

A compliance-ready CRM should help answer four questions fast:

| Compliance question | What the CRM should show |

|---|---|

| Who communicated with the client? | A dated interaction log tied to the contact record |

| What was said or shared? | Notes, archived messages, and linked materials |

| Who had access to the information? | Role-based permissions and user activity records |

| How long is the record preserved? | Retention rules connected to the record type |

Governance rules that hold up under review

Recordkeeping rules are not identical across channels, and that's where firms often slip.

Under the SEC marketing rule, records of adviser websites must be complete and accurate for at least five years from the end of the fiscal year in which the advertisement was last used. For communications governance, FINRA requires preservation of client communication, including emails and social media posts, for up to six years. Those retention windows should shape CRM-connected archiving rules from the start, not after launch.

Another hard boundary is content logic. The SEC Marketing Compliance Rule prohibits communications that predict or project performance, with narrow exceptions, and requires balanced presentation of risks and benefits. If a CRM triggers outreach, the content rules need to be embedded into templates, approvals, and escalation paths.

For firms tightening their underlying data controls, some of the same discipline used in broader martech data quality practices can be adapted to advisory and banking environments. The difference is that in financial services, bad data isn't just inefficient. It can become a supervision problem.

Clean data helps marketing. Governed data helps the firm survive an exam.

Must Have CRM Features for Regulated Firms

Feature lists get inflated quickly in CRM discussions. Most of that noise isn't useful. Regulated firms need a shorter list of capabilities that protect the business, support the team, and make compliant personalization possible.

Modern financial services CRMs integrate KYC and automated risk assessment capabilities, including identity verification, data encryption, and user activity monitoring, to ensure compliance with regulations like PCI DSS, GDPR, and SOX. That baseline should shape the evaluation process.

Non negotiable controls

Some features are not optional in financial services.

Integrated onboarding controls

The CRM should support a structured onboarding sequence with checkpoints for identity verification, document collection, approvals, and follow-up. If onboarding lives partly in email and partly in memory, errors multiply.Risk and suitability context

The system should maintain current client goals, risk tolerance details, and relevant financial profile information in a way that advisors and supervisors can use. This matters for both service quality and defensibility.Encryption and access management

Sensitive client records require protection in transit and at rest, plus controlled access by role. Permissions should match job function, not convenience.User activity monitoring

Firms need visibility into who changed records, who viewed sensitive information, and when key actions occurred. That's essential for internal accountability.

Features that support growth without creating compliance drag

The best CRM setups don't force firms to choose between personalization and control. They create boundaries that allow both.

A practical checklist looks like this:

Segmentation with guardrails

Teams should be able to group contacts by client type, lifecycle stage, service need, or planning milestone. But those segments should connect to approved content rules and review logic.Workflow automation with approval points

Automation is useful for reminders, task assignment, onboarding progress, review scheduling, and service follow-up. It becomes risky when firms automate messaging without supervision logic.Portfolio and account visibility

For investment-oriented firms, CRM records should connect to current holdings context, performance monitoring views, and account-level service cues so advisors can prepare intelligently.Life event tracking

A strong system gives staff a way to capture and act on milestones such as retirement, inheritance, business sale, divorce, or a child entering college. Those events often determine the next best service conversation.Documented communication history

The CRM should maintain a useful chronology of the relationship, not just a pile of disconnected notes. Staff should be able to see decisions, promises, questions, and unresolved issues in sequence.

A common mistake is trying to automate persuasion. That usually produces generic outreach that feels out of place in a trust-based business.

A better pattern is simple. Automate administration. Keep judgment human. Use the system to prompt the right conversation, not to impersonate one.

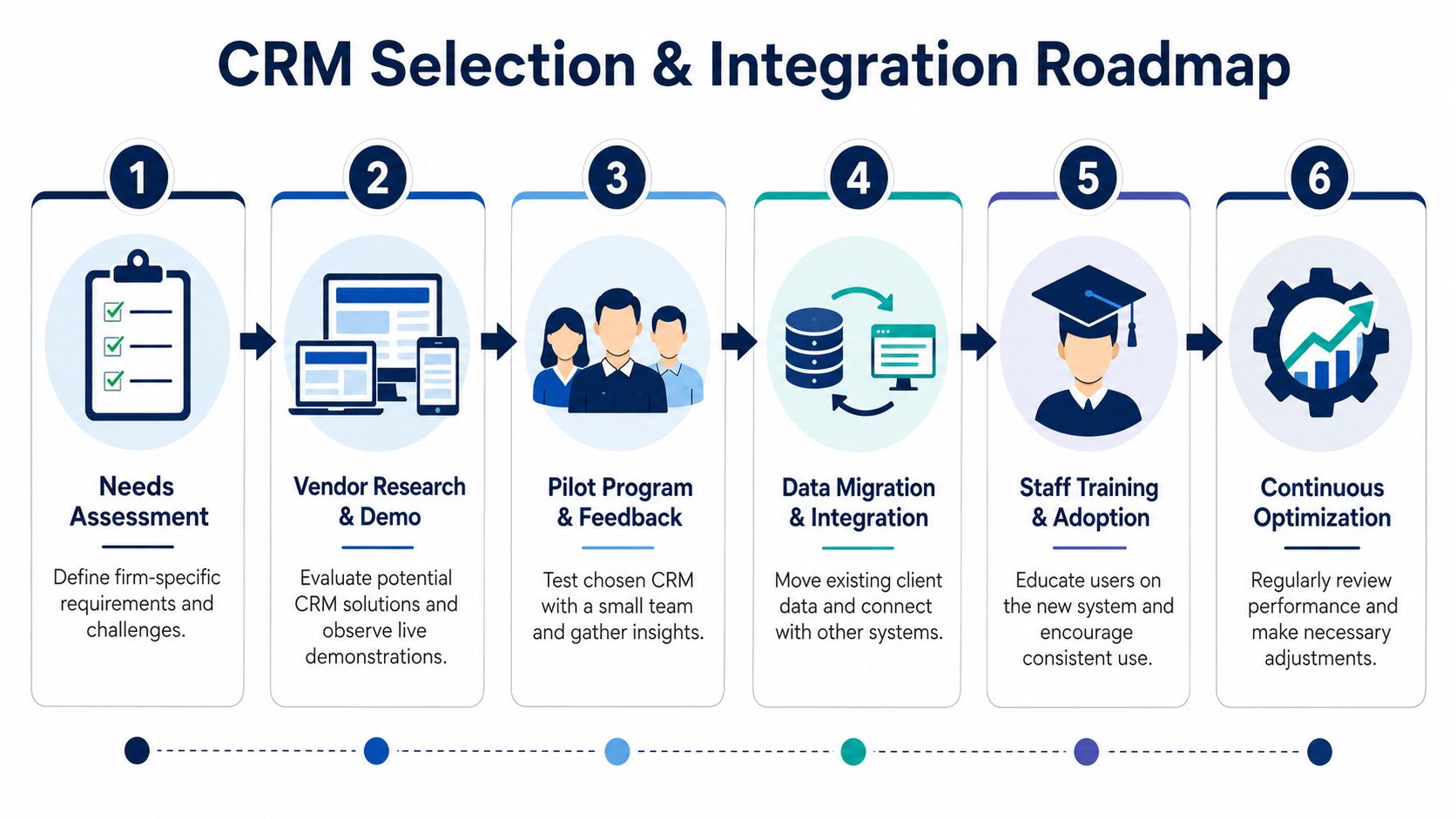

Selecting and Integrating Your CRM System

Firms often treat CRM selection like a software demo contest. That's backwards. Selection should start with business requirements, compliance constraints, and workflow pain points. Otherwise, teams buy a system that looks polished but doesn't fit the firm's real operating model.

Build the selection process before the demo

A practical vendor scorecard should cover these categories:

- Regulatory fit: Can the system support retention, permissions, audit history, and controlled workflows?

- Workflow fit: Does it match how the firm handles prospecting, onboarding, reviews, service tickets, and internal approvals?

- Integration fit: Can it connect cleanly to planning, communication, and operational systems already in use?

- Usability fit: Can advisors, service teams, operations, and compliance staff all use it without creating workarounds?

- Reporting fit: Does it produce usable visibility into open tasks, aging items, service bottlenecks, and supervisory needs?

A useful way to pressure-test workflow fit is to bring real scenarios into the evaluation. Ask the vendor to demonstrate a new lead assignment, a client onboarding checklist, a review meeting preparation workflow, a client complaint log, and a marketing approval path. Generic demos hide friction.

For firms that rely heavily on phone-based service or intake workflows, it also helps to understand how CRM design affects contact handling and recordkeeping. This overview of compliant call center software is useful for teams that need tighter integration between communication activity and supervised client records.

Rollout discipline matters more than feature volume

Implementation usually fails during migration and adoption, not procurement.

A sound rollout plan has six parts:

| Step | What matters |

|---|---|

| Needs assessment | Define the minimum data model and required workflows |

| Data cleanup | Remove duplicates, outdated records, and inconsistent field values |

| Pilot group | Test with a small team that will give blunt feedback |

| Integration build | Connect the CRM to necessary systems and validate record flow |

| Training by role | Teach advisors, operations, and compliance staff differently |

| Post launch review | Fix bottlenecks quickly before bad habits settle in |

Operational warning: Dirty migration creates a dirty future. If the legacy data is unreliable, moving all of it only scales the problem.

Phased rollout is usually the safer path. One team starts first. Core workflows get tested under real conditions. Exceptions are documented. Permissions are adjusted. Only then should the system expand across the firm.

This also helps with governance. It's easier to monitor whether required fields are being completed, whether tasks are being closed properly, and whether staff is documenting client interactions consistently when implementation happens in controlled stages rather than one large release.

Driving Adoption with Coaching and Change Management

Most CRM failures aren't technical. They're behavioral. The firm buys a capable system, sets up fields, migrates records, and launches training. Then usage drifts. Advisors keep shadow notes. Service staff logs only part of the interaction. Managers assume adoption happened because everyone attended the session.

That doesn't work in a regulated environment.

Why teams resist good systems

Resistance usually has a practical cause, not a philosophical one.

Sometimes the CRM asks staff to do extra data entry without showing a clear benefit. Sometimes fields don't reflect real workflows. Often the biggest barrier is compliance anxiety. Many guides overlook the fact that 68% of RIAs delay CRM implementation because they fear compliance violations in automated personalization. That fear is rational when firms introduce automation without clear rules.

Staff won't trust the system if they don't know:

- what can be automated

- what requires review

- what language is off limits

- what gets archived

- what records must be attached to the client file

How firms get consistent adoption

The firms that get value from CRM coaching treat training as an operating discipline, not a launch event.

Start with role-specific expectations. Advisors need to know how the CRM helps them prepare for meetings, track commitments, and move prospects through a compliant process. Operations needs clean task ownership and exception handling. Compliance needs confidence that records, approvals, and supervision points are happening.

A strong adoption plan usually includes:

- Internal champions: Pick respected users in different departments who can answer practical questions quickly.

- Usage standards: Define what a completed contact record, meeting note, task update, and onboarding file must contain.

- Manager review: Supervisors should inspect usage patterns, not just results.

- Coaching loops: Retrain around common failures such as weak notes, overdue tasks, or unlogged service activity.

For firms that need structured support on process improvement and team execution, practice management guidance like advisor coaching resources can help translate CRM expectations into daily operating habits.

Technology can standardize a process. Coaching is what makes people follow it consistently.

Another issue gets ignored too often. Human relationships still drive retention in financial services. Automation can organize the next action, but staff still need to listen well, ask better follow-up questions, and recognize when a client concern doesn't fit the script. If the firm automates outreach but never coaches empathy, the process becomes efficient and impersonal at the same time.

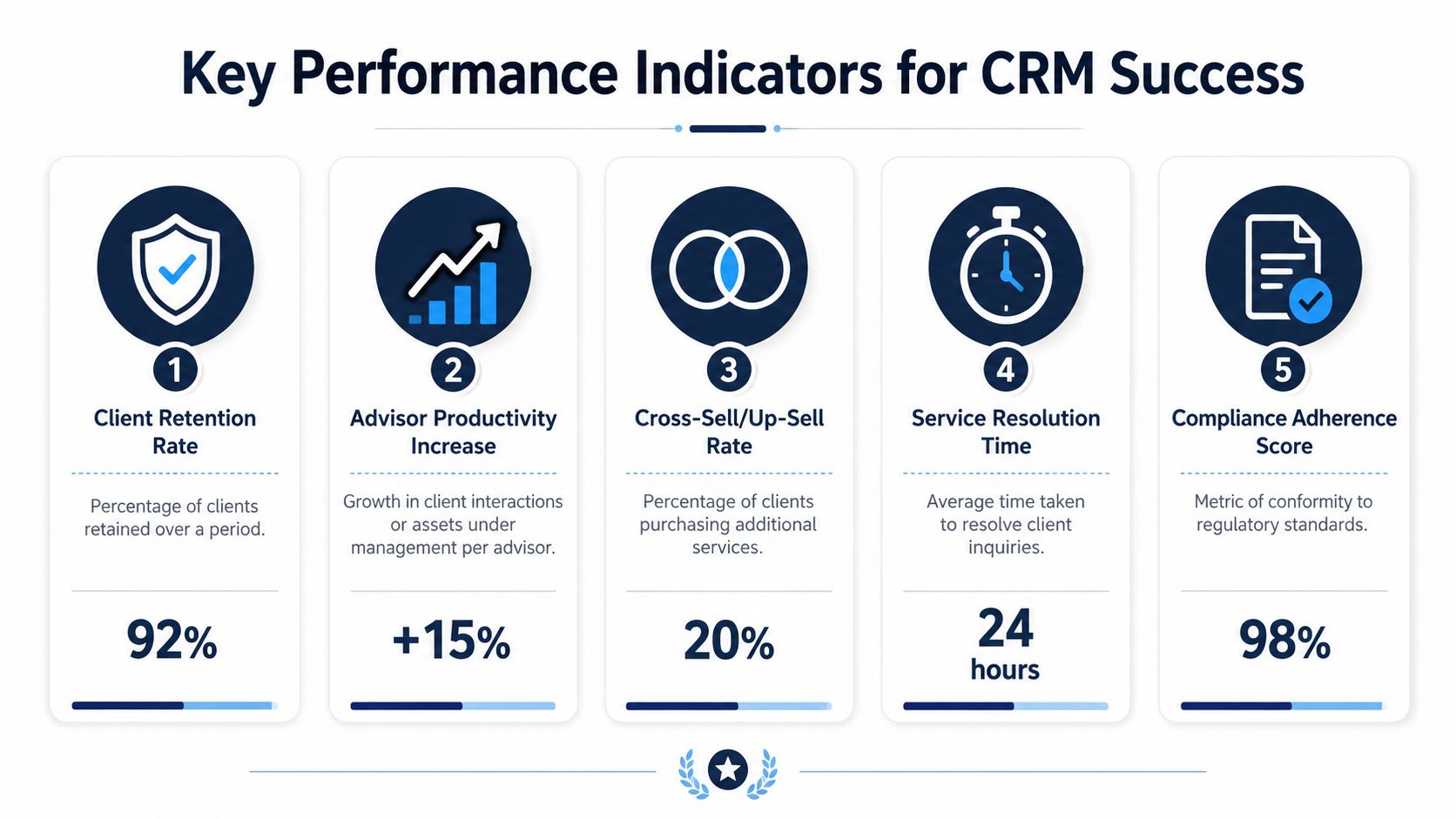

Measuring Success and Real World Examples

CRM success should be visible in behavior and outcomes. If the system is healthy, managers can see cleaner pipelines, fewer dropped tasks, more complete records, smoother onboarding, and less scrambling before audits or review meetings.

Metrics that show whether the system is working

The infographic above displays sample KPI values, but each firm should set its own baselines and targets based on its operating model. In practice, the most useful measures are usually:

- Lead conversion quality: Are prospects receiving timely follow-up and moving through a defined process?

- Onboarding cycle time: How long does it take to move from signed agreement to fully active service?

- Task completion discipline: Are promised follow-ups getting logged and closed?

- Client retention signals: Are review cycles, service requests, and life-event outreach happening consistently?

- Audit readiness: Can the firm retrieve a full communication and workflow record without manual reconstruction?

What improved operations looks like in practice

One advisory team may start with scattered inquiry handling. New leads come in, but no one owns the next step. After CRM rollout, each lead is assigned, tagged by source, and moved through a supervised follow-up sequence. Conversion improves because the team stops missing handoffs.

A banking or wealth management team may begin with weak documentation across departments. Service requests, product questions, and meeting notes sit in different places. After centralizing the record, staff can pick up the relationship without asking the client to repeat the story. Exam prep also becomes easier because the communication trail exists before anyone requests it.

The practical test is simple. A strong CRM should help the firm win business more cleanly, serve clients more consistently, and prove its process under scrutiny.

Advisor Momentum helps financial advisors, planners, and banking teams build compliant growth systems that connect marketing, service workflows, and coaching. Firms that need stronger lead conversion, tighter compliance-aware content processes, or better operational adoption can explore Advisor Momentum for support specific to regulated financial services.