A new advisor opens a client file and sees “CGA” in three different places over the same week. One appears on a résumé from a prospective hire. Another shows up in estate planning notes tied to charitable intent. A third sits in medical paperwork related to long term care discussions. The letters are the same. The meaning is not.

That small ambiguity can create real problems inside an advisory practice. A team can misread a credential, describe a planning strategy incorrectly, or route a client conversation to the wrong specialist. In a regulated business, that kind of confusion isn't just awkward. It can affect hiring decisions, marketing language, documentation, and client trust.

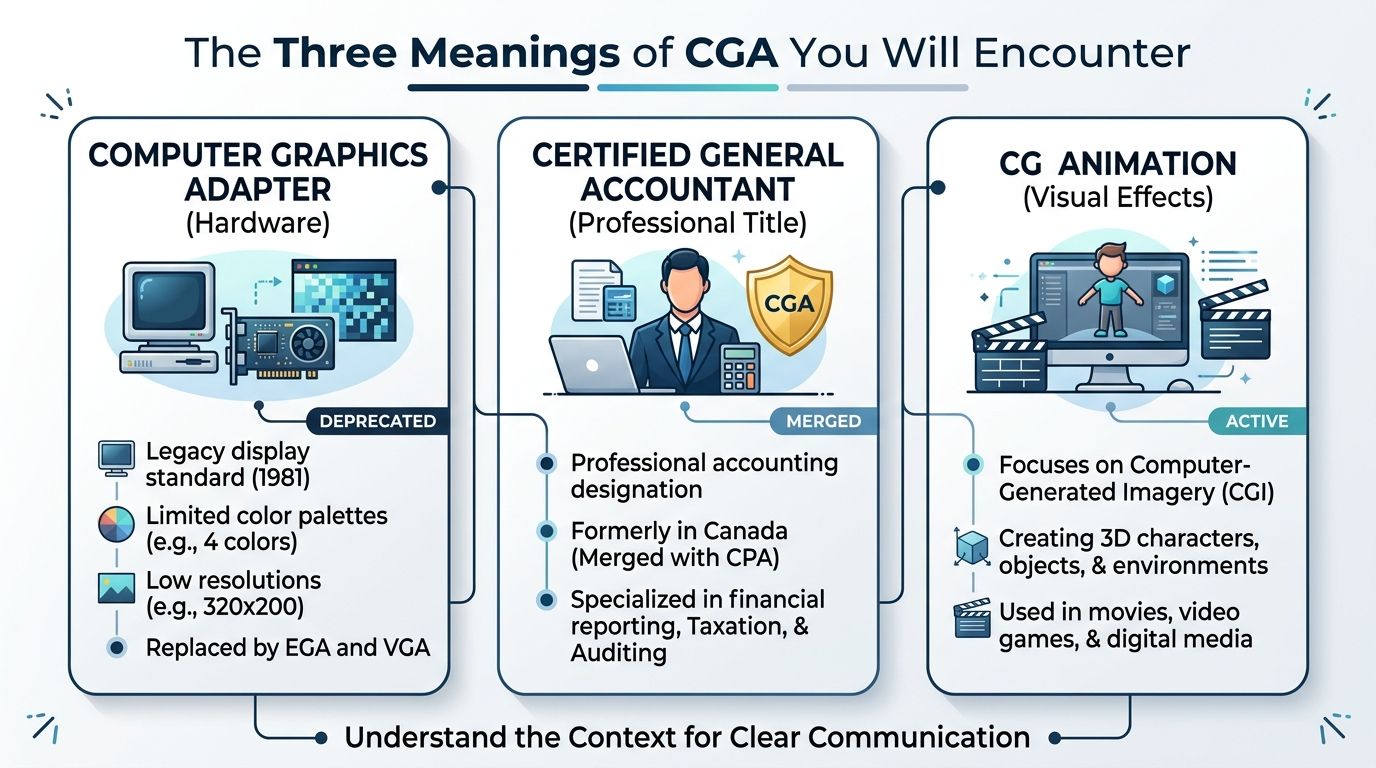

For advisors asking what is a CGA, the right answer starts with context. In most advisory settings, CGA usually means one of three things. Certified General Accountant, Charitable Gift Annuity, or Thorough Geriatric Assessment. Each points to a different domain, a different workflow, and a different next step.

Table of Contents

- The CGA Acronym A Common Point of Confusion

- The Three Meanings of CGA You Will Encounter

- CGA the Accountant Legacy and Modern Relevance

- CGA the Financial Tool A Guide to Charitable Gift Annuities

- Practical Steps When CGA Appears in Your Workflow

- Bringing Clarity and Compliance to Your Practice

The CGA Acronym A Common Point of Confusion

CGA is one of those acronyms that looks harmless until it lands in the wrong conversation. A banker may assume it refers to a financial product. A hiring manager may read it as an active accounting designation. A planning associate may see it in clinical paperwork and think it belongs in portfolio notes. None of those mistakes are unusual.

The practical fix is simple. Start by asking where the acronym appears and what job it is doing in that document. A résumé, donor illustration, and geriatric care report use language differently. The same three letters can signal a professional credential, a charitable income strategy, or a health assessment framework.

The first question isn't definition. It's context.

Advisors tend to get better answers when they stop asking “What does CGA mean?” and instead ask a narrower question.

- Where did it appear: résumé, client notes, tax document, medical file, or marketing draft.

- Who used it: accountant, attorney, client, physician, development officer, or recruiter.

- What decision depends on it: hiring, suitability review, referral, disclosure, or care planning.

Practical rule: If the acronym affects a recommendation, a hiring decision, or client-facing language, the team should verify the full term before taking the next step.

That sounds basic, but it prevents a lot of avoidable rework. A résumé with “CGA” should push the team toward credential verification and current licensure review. A client discussion about income for life and charitable intent should point toward annuity mechanics and tax treatment. A medical packet tied to aging, cognition, or care transitions should push the team toward planning sensitivity, not product explanation.

Why this matters inside a regulated practice

Ambiguous language creates downstream risk. Marketing teams can publish the wrong explanation. Advisors can promise a feature that belongs to a different meaning of CGA. Operations staff can file documents under the wrong category and make later review harder than it needs to be.

The stronger workflow is to treat CGA as a trigger for clarification. That one step supports cleaner notes, better handoffs, and more accurate communication with clients and centers of influence.

The Three Meanings of CGA You Will Encounter

Most advisory professionals will run into three meanings of CGA often enough to need a clean mental model. Two are directly tied to financial work. One matters because it appears in planning conversations around aging, capacity, and care.

The quick context test

Certified General Accountant refers to a legacy Canadian accounting designation. Before its obsolescence in 2014, the program had over 10,000 members working in public practice, industry, finance, and not-for-profit sectors across Canada. This meaning is most likely to appear on résumés, biographies, referral partner profiles, and older corporate records.

Charitable Gift Annuity refers to a planning arrangement involving a donor and a nonprofit. This meaning appears in charitable planning, retirement income discussions, estate conversations, and donor proposal materials.

Thorough Geriatric Assessment is a medical term. It usually shows up in care coordination, elder planning files, long term care conversations, and documents dealing with medical, psychological, or functional capability. It isn't an advisory product, but it can shape client needs and family decision-making.

If the document mentions taxes, charities, income payments, or gifting, think Charitable Gift Annuity first. If it mentions licensure, employment history, or accounting work, think Certified General Accountant. If it mentions function, cognition, or care plans, it likely belongs to a medical context.

CGA At a Glance Comparing the Three Meanings

| Aspect | Certified General Accountant | Charitable Gift Annuity | Comprehensive Geriatric Assessment |

|---|---|---|---|

| Domain | Accounting | Financial planning and philanthropy | Medical and care planning |

| Primary purpose | Professional credential and training path | Fixed income arrangement linked to a charitable gift | Multidimensional assessment of an older adult |

| Where advisors see it | Résumés, bios, partner credentials, legacy records | Estate plans, charitable planning notes, donor proposals | Health records, care planning documents, family files |

| Why it matters | Hiring, partnership evaluation, professional credibility | Retirement income, charitable intent, tax planning discussions | Capacity, family dynamics, long term care planning |

| Typical next step | Verify current status and role relevance | Review suitability, tax treatment, charity process, records | Coordinate carefully with client, family, and outside professionals |

The key operational point is that these meanings don't overlap in any useful way. Treating them as interchangeable wastes time and can create preventable errors in notes, marketing copy, and client conversations.

CGA the Accountant Legacy and Modern Relevance

When CGA appears on a résumé or professional bio, it usually points to Certified General Accountant, a former Canadian accounting designation. That title matters because it signals real accounting training, but it also requires current context. It is not the live path for new candidates today.

What the old designation meant

The legacy structure was broad rather than narrow. Candidates completed a bachelor's degree, the CGA Program of Professional Studies, and approved professional work experience. The designation was associated with accounting, taxation, auditing, and business advisory work across industry, commerce, government, and public practice.

The transition point is clear. The Certified General Accountant designation was replaced by the unified Certified Professional Accountant title in 2014, consolidating the former CGA, CMA, and CA paths into a single national framework in Canada. For an advisor reviewing credentials, that one fact answers the biggest question. A person can have a legitimate CGA background, but the title itself is part of a legacy framework.

What it means on a résumé today

A résumé that still lists CGA shouldn't be dismissed. It often signals a professional who trained under a recognized accounting pathway and then moved through the unification period. The stronger question isn't whether the old title existed. It did. The stronger question is whether the person also shows current standing, present role clarity, and, where relevant, modern licensure under the current framework.

That matters in hiring. A practice manager reviewing talent for operations, planning support, tax-aware service, or finance leadership should look at three things:

- Date context: Determine whether the credential reflects legacy education and experience from before the unification.

- Current status: Confirm how the person describes their present professional standing now.

- Role fit: Match the accounting background to the actual job. Strong accounting training doesn't automatically mean client-facing suitability.

A legacy credential can still signal present value. What matters is whether the candidate explains it clearly and accurately.

A team also needs to think about marketing and public biographies. If a staff member or referral partner uses CGA in outward-facing materials, the language should be precise enough that a U.S. prospect doesn't mistake it for a product, a medical term, or an active domestic license category. Clear wording reduces friction before compliance ever gets involved.

For firms building hiring pipelines, good process matters more than broad assumptions. A credential review step, a standardized bio template, and role-specific screening questions tend to produce better outcomes than relying on acronym recognition. Practices that want a more structured way to build talent standards often benefit from clear financial advisor training programs so titles, qualifications, and actual job expectations stay aligned.

CGA the Financial Tool A Guide to Charitable Gift Annuities

In client work, CGA often means Charitable Gift Annuity. This is the meaning that requires the most care because clients may hear “annuity,” “charitable deduction,” and “income for life” and assume the strategy is simpler than it is.

How the arrangement works

A Charitable Gift Annuity is a contract where a donor transfers assets to a nonprofit in exchange for a fixed income stream for one or two lives, backed by the nonprofit's entire asset base. For an advisor, the plain-English version is straightforward. The client makes an irrevocable gift and, in return, the nonprofit promises fixed payments for life.

The fixed nature of the payment is the practical attraction. Clients who value predictability often respond well to that feature. The charitable side is the emotional and planning side. The client supports a mission they care about while also creating a defined income stream.

The tax treatment is where advisors need to explain carefully. The transaction is treated as a bargain sale. The easiest analogy is this: part of what the client transfers functions like a gift, and part functions like the purchase of an income interest. That split is why the planning discussion can't stop at “you give assets and get payments.”

Where advisors need to slow down

Not every funding source behaves the same way. For donors age 70½ or older, there is a one-time transfer option from a traditional IRA to a CGA, with a maximum funding limit of $54,000 in 2025, adjusted annually for inflation, according to guidance on charitable gift annuity tax rules. The same source notes that cash-funded CGAs provide no charitable deduction and that all payments are taxed as ordinary income to the annuitant.

That alone should change how an advisor frames the conversation. “CGA” is not a plug-and-play recommendation. The source of funds, the client's charitable intent, tax posture, liquidity needs, and time horizon all matter.

A practical review often includes these questions:

- Why this client wants it: Is the goal philanthropy, stable income, or both.

- What asset is being used: Cash, appreciated property, or an eligible IRA transfer create different planning consequences.

- How soon income is needed: A client asking for immediate retirement cash flow should be handled differently from a client focused on long-term mission support.

- Which charity is involved: The charity's administrative strength and communication process matter because the contract is irrevocable.

The 2026 conversation adds another wrinkle. One underserved point in advisor education is how the projected 2026 IRA-to-CGA $55,000 limit interacts with the $111,000 Qualified Charitable Distribution cap, as discussed in this overview of how charitable gift annuities work. That issue matters for older clients trying to balance charitable planning with required distribution strategy. Advisors shouldn't gloss over it or collapse it into a generic QCD conversation.

The wrong way to present a Charitable Gift Annuity is as a yield product. The right way is to present it as a charitable contract with income features and tax consequences that need careful review.

Practical Steps When CGA Appears in Your Workflow

Most confusion around CGA disappears once a practice uses the same intake and verification method every time. Ambiguity becomes manageable when staff know what to check, who to ask, and how to document the answer.

A working protocol for advisors

A simple workflow beats a clever one. When CGA appears anywhere in the business, the team should pause and classify it before moving it into planning, marketing, or operations.

- Read the surrounding language first. A résumé, donor letter, and care report each create different assumptions. Staff should identify the document type before they try to define the acronym.

- Expand the term in writing. In CRM notes, internal email, or review comments, the team should write the full phrase once. That prevents later confusion when another person picks up the file.

- Route by function. Accounting credentials go to hiring or partner review. Charitable annuity references go to planning and compliance review. Medical references go to the advisor handling family communication and care-sensitive planning.

- Record the basis for interpretation. Short notes matter. “CGA used in donor illustration” is better than “CGA discussed.”

That process works because it creates consistency. New advisors don't need perfect acronym recall. They need a repeatable rule.

Where compliance and marketing intersect

The compliance side becomes concrete when CGA refers to a Charitable Gift Annuity inside an RIA workflow. If the annuity is part of the advice process, the firm needs records that show what was reviewed, how the recommendation was discussed, and what documents supported the planning decision. Under SEC Rule 204-2, RIAs must retain client agreements, financial transaction records, and documentation of investment decisions for a minimum of five years from the end of the fiscal year in which the record was created.

That doesn't mean every CGA discussion becomes a paperwork exercise. It means the firm should preserve the materials that matter.

- Client communications: Save emails, meeting summaries, and recommendation notes when the CGA affects advice.

- Decision support: Retain illustrations, charitable planning memos, and the rationale used in the recommendation.

- Final documentation: Keep signed agreements and any related transaction records in the same accessible file set.

Marketing teams need similar discipline. If a website, brochure, or advisor bio uses “CGA,” the wording should be specific enough that a prospect doesn't misread it. Firms also need required website disclosures. A compliance-friendly adviser website should include the firm's name and contact information, Form CRS, applicable performance advertising or testimonial disclosures, and a statement that the firm is a registered investment adviser only where registered or exempt and that the material is for educational purposes, as outlined in guidance for building a compliance-friendly adviser website.

Clean language does double duty. It makes the prospect experience better, and it gives compliance fewer avoidable problems to fix later.

The same principle applies to hiring. If a recruiter or office manager sees CGA on an applicant profile, they should avoid assumptions and ask for current credential wording. Legacy designations should be described accurately in offer materials, public bios, and organizational charts.

Bringing Clarity and Compliance to Your Practice

Acronym confusion looks minor until it touches client advice, talent evaluation, or published marketing. Then it becomes an operations problem. CGA is a good example because each meaning points to a completely different action. One belongs to credential review. One belongs to charitable planning. One belongs to care-sensitive client context.

The firms that handle this well don't rely on memory alone. They use plain language, disciplined note-taking, and a review process that asks what the acronym means in that exact setting. That approach improves service and lowers preventable risk.

It also fits a wider practice standard. Clear communication around client data, documentation, and public-facing language should sit alongside basics like effective cybersecurity for small businesses, because both protect trust in ordinary day-to-day operations. On the client experience side, firms that define terms clearly and train staff to verify context usually create smoother handoffs and stronger advisor customer service.

Precision isn't a style preference in wealth management. It's part of competent practice.

Advisor Momentum helps financial advisors, RIAs, and banking teams build compliant marketing, stronger operations, and better growth systems. For firms that want support with advisor recruiting, website content, training, branding, or service workflows, Advisor Momentum provides industry-specific execution built for regulated financial organizations.