87% of support teams say customer expectations increased over the past year, 46% of customers expect a reply within four hours, and 63% rank speed of response as the most important factor according to customer service expectation data collected by Salesmate. For advisors, that changes the job. Client service is no longer a soft skill sitting next to planning and portfolio work. It is part of the operating model.

In a regulated firm, advisor customer service has to do two things at once. It has to feel personal, fast, and reassuring to the client. It also has to hold up under supervision, retention, and audit requirements. That means the service workflow can't live in scattered inboxes, personal texts, and unwritten habits. It has to be built deliberately, with communication rules, documentation standards, and escalation paths tied directly to the client experience.

Many firms still separate service from compliance. That split creates avoidable risk. A welcome email, a scheduling text, a market-volatility check-in, and an inherited account transfer are all service moments. They are also regulated communications. The firms that handle this well don't bolt compliance on after the fact. They embed it into onboarding, follow-up, documentation, and review.

Table of Contents

- Why Exceptional Advisor Service Is No Longer Optional

- Mapping The Compliance Aware Client Journey

- Operationalizing Service With Roles and Communication Protocols

- Building Your Advisor Service Tech Stack

- Measuring Success and Maintaining Compliance

- Fostering a Culture of Service Excellence

Why Exceptional Advisor Service Is No Longer Optional

Advisory firms often talk about service as if it's a relationship benefit that sits outside growth. That view is outdated. When clients expect fast acknowledgment and clear communication, service quality directly affects retention, referrals, and whether a prospect ever becomes a client in the first place.

The economics are hard to ignore. Poor customer experiences cost businesses globally an estimated $3.7 trillion annually, while 89% of consumers are more likely to make another purchase after a positive customer service experience according to customer service and loyalty research summarized by Nextiva. In financial advice, the product is trust under uncertainty. A delayed response during onboarding, a vague answer during a transfer, or silence during market stress doesn't feel like an operational miss to the client. It feels like a judgment problem.

The old service model breaks under pressure

The traditional advisory model relied on a small number of touchpoints, a lot of advisor memory, and an assumption that clients would tolerate delay if the relationship felt strong enough. That doesn't hold up now.

Clients compare their advisory experience to every other service interaction they have. They don't separate wealth management from the rest of digital life. They expect responsiveness, visibility, and clear next steps. A useful way to think about this is through a broader customer experience strategy for B2B, then adapt it to the regulatory and emotional reality of financial advice.

Practical rule: If a client has to wonder who owns the next step, the service model is already underperforming.

Firms that treat service as a revenue lever work differently. They define response standards, document handoffs, and remove ambiguity from recurring interactions. Firms that don't usually depend on heroic effort from one advisor or one operations person. That works until someone is out, inbox volume spikes, or a complex life event exposes the gaps.

Service quality drives business quality

A strong advisor customer service model does more than keep clients happy. It improves handoffs, reduces avoidable rework, and creates cleaner records. That matters for operations and for oversight.

A simple contrast makes the point clearer:

| Service habit | What clients feel | What firms deal with internally |

|---|---|---|

| Ad hoc replies from multiple channels | Uncertainty | Missed follow-up, inconsistent records |

| Clear routing and response rules | Confidence | Better workflow control |

| Generic check-ins | Low relevance | Weak engagement |

| Segment-specific communication | Understood and supported | Better retention conditions |

The firms gaining ground aren't always the firms with the biggest teams. They're the firms with a repeatable service system that clients can feel and compliance can defend.

Mapping The Compliance Aware Client Journey

A firm can't improve advisor customer service until it sees the experience the way a client does. Most firms map tasks. Fewer map emotions, communication risk, and documentation requirements at the same time. In regulated advice, those pieces belong on one map.

The journey starts before a prospect signs anything. It begins with the first website visit, the first inquiry form, the first call, and the first message confirming what happens next.

Start with the client's real experience

One of the biggest service mistakes in wealth management is assuming all clients need the same cadence, the same tone, and the same explanations. That especially breaks down with clients navigating emotionally loaded transitions. This discussion of how women investors are often underserved highlights a common failure point. Generic support models often overlook life circumstances such as widowhood or inheritance, and trust improves when advisors lead with empathy and listening rather than assumptions.

A journey map should therefore include more than milestones. It should identify where anxiety rises, where decisions stall, and where generic communication would feel dismissive.

A practical map should answer these questions:

- Entry point: How does the prospect first reach the firm, and what acknowledgment do they receive?

- Risk moments: Where are the points of confusion, delay, or emotional strain?

- Channel choice: Which interactions happen by phone, portal, email, or meeting?

- Recordkeeping impact: Which moments create communications that must be captured and reviewed?

- Ownership: Who is accountable for each next step?

Map five stages, not just meetings

Many firms benefit from using the same broad progression they already know from the stages of financial planning, but with service and compliance layers added to each stage.

Initial contact and qualification

Record how inquiry response works, who follows up, what information is gathered, and how expectations are set. This stage often reveals the first service gap. A prospect asks a direct question and receives a warm but vague reply with no timeline.Onboarding and account setup

List each required communication, including document requests, identity steps, custodial coordination, and timeline updates. Then mark which of those messages require approved language.Planning and advice delivery

Identify points where clients need education, reassurance, and summary follow-up. At these points, jargon and assumption-heavy communication often increase client effort.Ongoing servicing

Include routine reviews, beneficiary updates, contribution changes, transfer requests, and life-event outreach. Service consistency usually breaks here if the firm relies on advisor memory alone.Exception handling

Add a separate path for widowhood, inheritance, complaints, urgent cash needs, and market-driven concern. These aren't edge cases. They are trust-defining moments.

A compliance-aware journey map should show what the client hears, what the team does, and what the firm must retain.

When the map is complete, weak spots become obvious. A firm may discover that onboarding feels polished but post-meeting follow-up is inconsistent. Another may find that service standards exist for new assets but not for beneficiaries, inherited accounts, or client family members suddenly involved in decisions. Those are service design problems, not isolated incidents.

Operationalizing Service With Roles and Communication Protocols

A journey map is useful only when someone can execute it without guesswork. That requires role clarity, channel rules, and written communication standards. In advisor customer service, dropped balls usually come from shared responsibility with no true owner.

Assign ownership before issues appear

The cleanest service teams define who owns acknowledgment, who owns fulfillment, and who approves exceptions. That sounds simple, but many firms still assign all three to the advisor by default. The result is predictable. Clients wait too long for routine updates, operations staff hesitate to communicate, and nobody knows when a matter should escalate.

A stronger structure often includes:

- Advisor ownership for advice and relationship judgment: Reviews, recommendations, sensitive life-event conversations, and escalations.

- Service ownership for workflow progress: Scheduling, document follow-up, transfer status updates, account maintenance coordination, and routine confirmations.

- Compliance or supervisory ownership for exceptions: Complaints, advertising-related language, off-channel communication issues, and retention concerns.

This division improves service because it removes silence. The client hears from the right person sooner, and the team isn't waiting for one overloaded advisor to manage every touchpoint personally.

Build scripts that support judgment

Scripts have a bad reputation because firms often write them badly. A useful script doesn't make people sound robotic. It standardizes facts, required disclosures, and next-step framing while leaving room for human judgment.

For example, a good onboarding template should include acknowledgment, expected timeline, required documents, secure submission method, and who to contact with questions. A volatility-response template should avoid predictions, confirm review timing, and invite conversation without drifting into off-the-cuff commentary. A scheduling message should state purpose, timing, and channel while keeping the record clean.

Operational note: The script should carry the compliance burden for routine language so the team can focus attention on the client.

Communications rules don't stop at email. Under SEC Rule 204-2 communication retention requirements for RIAs, firms must retain all business communications, including email, text messages, and social media interactions, for a minimum of five years, even when the communication occurred on a personal device. That means service protocols must define approved channels, not just preferred ones.

A workable communication protocol usually covers three areas:

| Protocol area | Good practice | What fails |

|---|---|---|

| Channel use | Approved channels by message type | Personal texting for convenience |

| Templates | Pre-reviewed language for recurring scenarios | Free-form replies to sensitive matters |

| Escalation | Clear triggers for supervisor or advisor review | Team members improvising under pressure |

The point isn't to restrict communication. It's to make communication reliable, reviewable, and consistent. In regulated advice, a message that can't be retained or supervised isn't just a service problem. It's a control failure.

Building Your Advisor Service Tech Stack

Technology choices shape service quality more than most firms admit. The key question isn't whether a firm has software. It's whether the systems reduce friction, preserve context, and support compliant communication without forcing the team into workarounds.

Choose systems by capability, not by category label

A useful service stack creates one operating environment for people, records, and follow-up. That usually starts with a client relationship system that acts as the firm's working memory. For advisors thinking through structure, this overview of client relationship management for financial services is a practical reference point.

The capability checklist matters more than the product label. A firm should ask whether the stack can:

- Preserve conversation history: The team should see prior touchpoints without searching across inboxes.

- Route work visibly: Tasks, handoffs, and status updates shouldn't depend on memory.

- Support approved communication paths: Staff shouldn't need side channels to move quickly.

- Trigger reminders and recurring outreach: Routine servicing should happen by system, not by chance.

- Store evidence of service delivery: Notes, updates, and timestamps should be easy to retrieve.

A common failure pattern is buying separate systems that each do one thing well but don't support the service process end to end. That creates duplicate entry, conflicting records, and a fragmented client experience.

Technology should reduce client effort

The best advisor customer service stack lowers the amount of work a client has to do to get a clear answer. That means fewer repeated requests for the same document, fewer status-check emails, and fewer moments where the client has to ask, "What happens next?"

Service-enabling technology often earns its value in plain ways:

- Client portals reduce back-and-forth around documents and status visibility.

- Scheduling workflows cut delays and help standardize appointment preparation.

- Centralized knowledge bases give staff approved language and consistent process steps.

- Website and content systems help set expectations before the first conversation begins.

For firms that need support tying service workflows to digital experience and regulated messaging, Advisor Momentum is one option that provides compliance-ready website, content, and coaching support designed for financial advisory firms.

A tech stack should remove avoidable effort for both the client and the team. If it creates more side work than it eliminates, it isn't supporting service.

Technology is an investment when it protects continuity. If a key employee leaves, the service model should still function. If a client calls with a question after a transfer or beneficiary update, the team should have the full context in front of them. That's not convenience. It's operational resilience.

Measuring Success and Maintaining Compliance

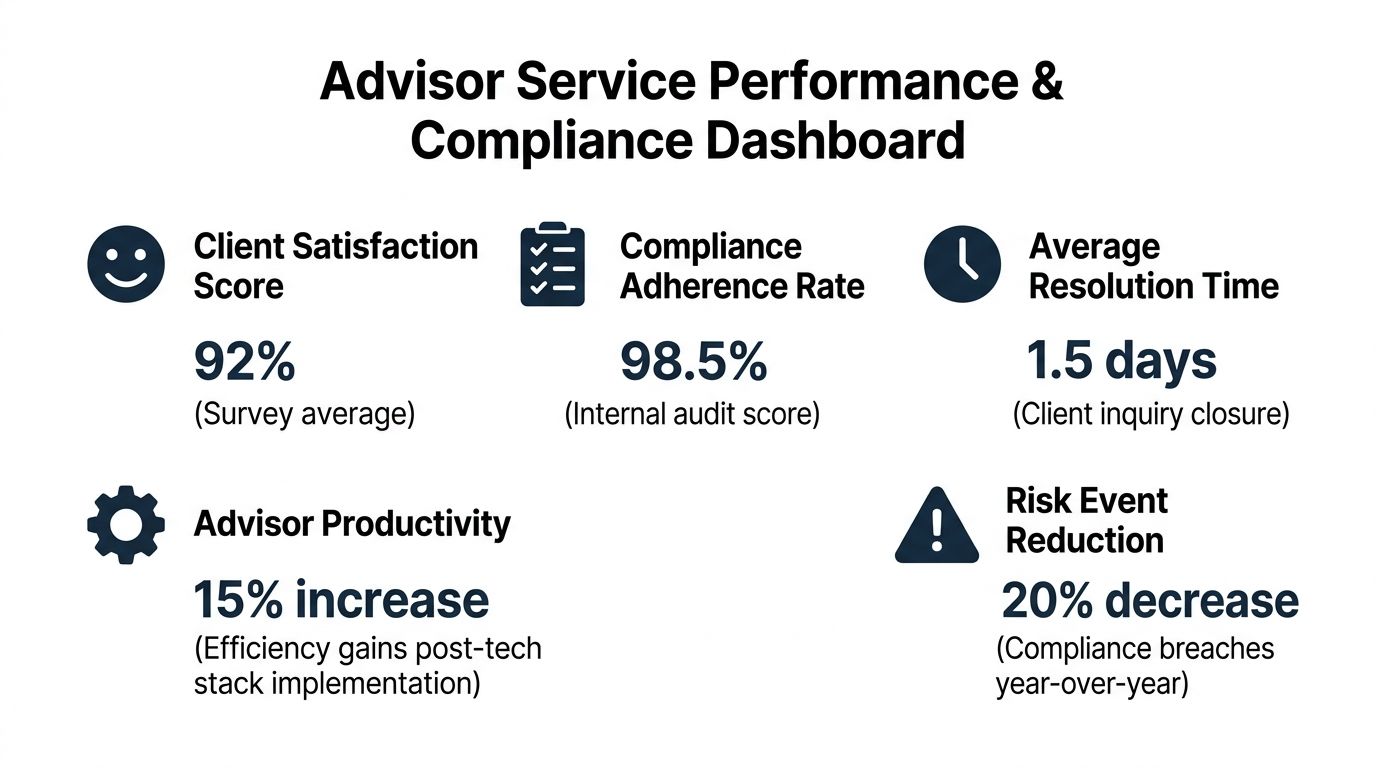

Service isn't managed by instinct alone. It needs operating metrics and review evidence. In advisory firms, measurement has to answer two questions at once. Is the client experience improving, and can the firm prove that communications and workflows followed policy?

Track service quality and audit readiness together

A practical service scorecard uses a small set of metrics linked to specific service pillars. A proven methodology described in this customer service standards framework starts with SMART goals and maps them to measures such as First Response Time, Average Resolution Time, First Contact Resolution, Customer Satisfaction, Customer Effort Score, and Net Promoter Score. That same source notes that CSAT scores above 80% are generally considered good.

For advisory firms, those metrics become more useful when paired with compliance evidence.

- First Response Time: Measures how quickly the firm acknowledges the client.

- First Contact Resolution: Shows whether the team solves routine issues without unnecessary back-and-forth.

- Customer Satisfaction: Tests whether the experience feels clear, timely, and respectful.

- Communication capture rate: Confirms the firm is retaining the channels it allows staff to use.

- Exception review rate: Tracks how consistently complaints, escalations, and sensitive communications are reviewed.

A firm doesn't need dozens of dashboards. It needs a short list of metrics that produce action. If response times are acceptable but satisfaction drops, the issue may be tone, clarity, or ownership. If satisfaction looks fine but communications are fragmented across channels, the firm may have a compliance problem hiding inside a service process.

Use reviews to correct process drift

Retention standards make this more than a service conversation. According to FINRA-aligned communication retention guidance summarized by StarCompliance, the SEC mandates a five-year retention period for RIA communications, while FINRA requires client communications including emails, newsletters, and social media posts to be kept for up to six years. Firms that supervise service well build reviews around that reality.

A simple monthly review can examine:

| Review area | What to inspect | Why it matters |

|---|---|---|

| Response samples | Tone, clarity, escalation use | Protects client experience |

| Channel adherence | Whether staff stayed on approved channels | Supports retention and supervision |

| Repeat contacts | Same issue reopened or re-explained | Reveals process failure |

| Disclosure and record evidence | Required wording and archived copies | Supports audit readiness |

For firms building or refreshing those controls, broader references on essential compliance for SMBs can help frame how documentation, verification, and operating discipline fit together, even though advisory firms need a more specific supervisory model.

Firms don't maintain compliance by writing policies once. They maintain it by reviewing what staff actually sent, where they sent it, and whether the record exists.

The strongest measurement systems also loop findings back into templates, training, and workflow design. When repeated confusion shows up in one onboarding step, the fix should be operational, not motivational. Rewrite the message, adjust the handoff, and clarify ownership.

Fostering a Culture of Service Excellence

A service playbook works only when the team uses it with judgment and consistency. Culture is what determines whether protocols become habits or just binders on a shelf. In advisor customer service, culture isn't about slogans. It's about whether people understand the standard, practice the standard, and see that leadership reinforces the standard.

Train for judgment, not script recitation

Teams need scenario-based coaching because real client conversations rarely arrive in clean categories. A widow calling about inherited assets needs empathy and process clarity. A frustrated client asking why a transfer is delayed needs acknowledgment, ownership, and a documented next step. A team member who has practiced those moments will respond differently than one who has only read procedure notes.

Useful training usually includes:

- Role-play for high-emotion events: Inheritance, death, complaints, urgent withdrawals, and market stress.

- Workflow drills: How to log the interaction, trigger follow-up, and route exceptions.

- Message review sessions: Compare strong and weak versions of common client replies.

- Supervisory refreshers: Reinforce approved channels, retention expectations, and escalation rules.

A broader service team can also borrow ideas from operational coaching in adjacent environments. This resource on optimizing call center performance is helpful for thinking about coaching cadence, workflow discipline, and response quality, even though advisory teams need a more specialized compliance overlay.

"Train the team on the moments that create anxiety, not just the steps that create paperwork."

Make accountability visible and fair

People usually support service standards when they can see how success is measured and when expectations are realistic. The same methodology noted earlier recommends setting SMART goals around metrics like First Contact Resolution and Customer Satisfaction, with CSAT above 80% generally considered good in that framework. Those targets work best when translated into team-level behaviors rather than posted as abstract numbers.

That means managers should connect metrics to observable habits:

- For responsiveness: Did the client receive acknowledgment promptly and clearly?

- For resolution quality: Did the team answer the actual question and define the next step?

- For consistency: Did the staff member use the approved workflow and channel?

- For empathy: Did the communication fit the client's situation, or did it sound generic?

Culture improves when managers review examples, not just scores. A low-quality interaction should lead to coaching and process correction. A strong interaction should be saved, anonymized, and used as a teaching model.

Service excellence in an advisory firm is never just hospitality. It is professionalism expressed through timing, clarity, empathy, and record discipline. When those elements align, clients feel taken care of and the firm becomes easier to supervise.

Advisor Momentum helps advisory firms build compliant service systems that connect digital presence, client communication, and operational workflow. For firms that want tighter onboarding, cleaner messaging, and stronger service consistency without separating marketing from compliance reality, Advisor Momentum is a practical resource.