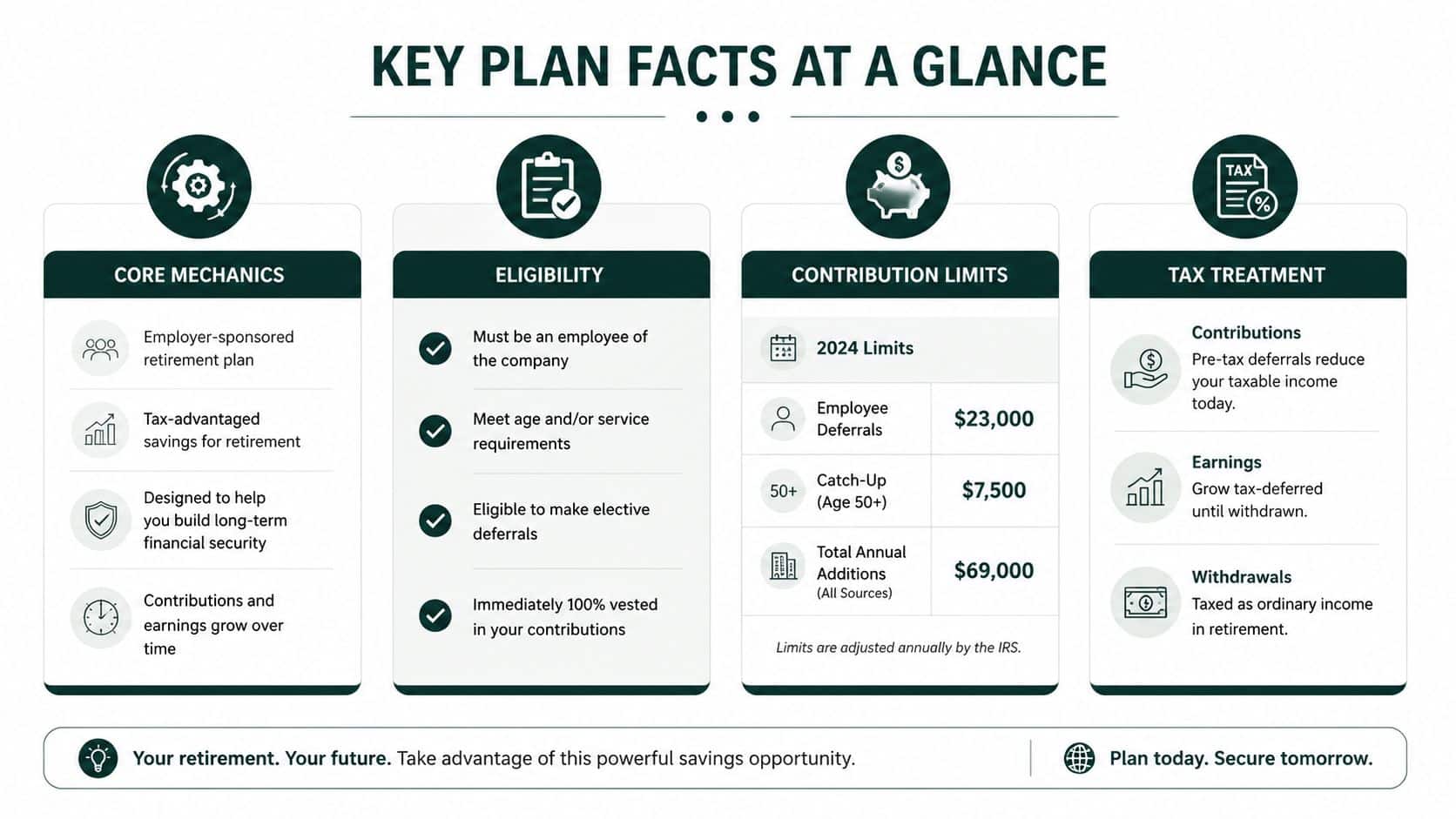

A 403(b) is a retirement plan for employees of public schools, universities, churches, and 501(c)(3) organizations, and in 2026 the standard employee contribution limit is $24,500. Workers age 50 and older can generally add $8,000, and those ages 60 to 63 can qualify for a higher $11,250 catch-up if the plan allows it.

A financial advisor often meets this question in a familiar setting. A new client joins the firm from a school district, hospital system, university, or nonprofit and arrives with an old account statement, several vendor names, and a basic question that sounds simple but rarely is: 403 b what is it, and how should it fit into the broader plan?

The simple answer is that a 403(b) is the non-profit and public education sector's version of a 401(k). The difficult part is that the similarities can hide the rules that matter most in real client advice. Eligibility is narrower. plan structure can differ dramatically. Investment menus may reflect an annuity legacy. Compliance obligations change depending on whether the arrangement is ERISA or non-ERISA. For 2026, a Roth catch-up rule for higher earners adds another layer that many clients, and some advisors, still miss.

That's why a basic definition isn't enough. Financial professionals need a working understanding of contribution mechanics, investment architecture, withdrawal rules, rollover implications, and the compliance flags that can create planning errors. Advisors refining their service model can also benefit from stronger process design, especially when retirement plan analysis connects with broader financial planning workflow stages.

Table of Contents

- Introduction What Is a 403(b) and Why It Matters for Your Practice

- Core Mechanics Eligibility Contribution Limits and Tax Treatment

- Investment Structures Annuities and Custodial Accounts

- 403(b) vs 401(k) A Strategic Comparison for Client Planning

- Navigating Distributions Rules for Withdrawals and Rollovers

- ERISA vs Non-ERISA Critical Compliance Nuances for Advisors

- Frequently Asked Questions from Financial Advisors

Introduction What Is a 403(b) and Why It Matters for Your Practice

A teacher calls after accepting an offer from a new district. She has been contributing to a 403(b) for years, assumes it works just like her spouse's 401(k), and wants to know whether she should roll it over, keep it in place, or increase deferrals before the move. That conversation sounds routine. It often is not.

For advisors, a 403(b) deserves closer scrutiny because small classification errors can lead to flawed recommendations. The IRS describes a 403(b) as a retirement plan for employees of public schools, certain ministers, and many employees of tax-exempt organizations under Section 501(c)(3), with rules set out under Internal Revenue Code Section 403(b) and related guidance on retirement plan contribution stages and planning decisions. On the surface, that puts it in the same broad family as other salary-deferral plans. In practice, 403(b) cases often involve different plan histories, different administrative realities, and different compliance questions.

A 403(b) works like a familiar workplace retirement account, but the wiring behind the walls can differ.

That distinction matters in advisory work. A hospital executive employed by a nonprofit system may have a very different planning profile from a public school administrator, even if both say, “I have a 403(b).” One plan may have stronger employer involvement and ERISA oversight. Another may be a non-ERISA arrangement with limited employer discretion, multiple legacy contracts, and a recordkeeping trail that requires careful verification before any rollover or consolidation advice.

Advisors can add real value. General consumer explanations usually stop at “tax-advantaged retirement plan for nonprofit and education employees.” Useful, but incomplete. The better advisory question is narrower and more practical: what kind of 403(b) is this, who controls it, what compliance rules apply, and what planning options are available to this client right now?

A strong opening review usually centers on three facts:

- The sponsoring employer sets the frame. Public schools, tax-exempt organizations, and certain religious employers can create 403(b) opportunities, but the employer category often signals which planning and compliance issues deserve immediate attention.

- Plan design can vary more than clients expect. Two participants with 403(b) accounts may face very different vendor arrangements, account types, and administrative constraints.

- Advisor risk rises when assumptions replace document review. ERISA status, legacy contracts, and upcoming high-earner Roth catch-up rules for 2026 can all change the advice path.

For professionals serving educators, nonprofit executives, clergy, and physicians in tax-exempt systems, understanding 403(b) plans is not just a matter of product knowledge. It is part of giving advice that is accurate, defensible, and appropriate for the rules that govern the account.

Core Mechanics Eligibility Contribution Limits and Tax Treatment

A school administrator joins your calendar and says, “I have a 403(b), so I can put in the same amount my colleague does, right?” That question sounds simple. In practice, it can expose three separate review points that advisors cannot afford to blur together: who is eligible to participate, which contribution limit applies to this specific employee, and whether deferrals should be traditional, Roth, or split between both.

Who can participate

Eligibility starts with the employer's status under the tax code and then narrows to the terms of the plan. 403(b) arrangements are generally associated with public schools, certain tax-exempt organizations, and some church-related employers. For advisors, that means intake should begin with employer classification, not with the client's account statement.

Then comes the second layer. A client may work for a qualifying organization and still face plan-specific entry rules, excluded classes, or administrative delays before salary deferrals begin. Universal availability rules can also create compliance questions in elective deferral plans, especially if the employer's enrollment practices are inconsistent. That is one reason a 403(b) should never be treated as a generic nonprofit version of a 401(k).

A useful review usually covers:

- Employer type: Confirm that the organization falls within a category permitted to sponsor a 403(b).

- Current plan entry status: Verify whether the employee is eligible now, recently became eligible, or was improperly left out.

- Contribution types available: Confirm whether the plan permits pre-tax deferrals, designated Roth deferrals, or both.

- Plan governance clues: Note facts that may later matter for ERISA analysis, document requests, and participant disclosures.

That last point matters more than many clients realize. A contribution recommendation can be technically correct and still be poorly timed if the advisor has not confirmed how the plan is administered.

How much a client can contribute in 2026

Contribution limits in 403(b) plans work like stacked shelves. One shelf is the standard elective deferral limit. Additional shelves may be available for age-based catch-up contributions and, in some cases, the special 15-years-of-service catch-up under section 403(b). If you place the client on the wrong shelf, the advice can drift into excess deferral territory.

For 2026, the IRS increased the basic elective deferral limit to $24,000, as shown in IRS Notice 2025-68. The same notice lists the general age 50 catch-up at $8,000 for 2026.

Advisors also need to account for the newer higher catch-up window for participants ages 60 through 63, if the plan permits it. Under the SECURE 2.0 changes reflected in IRS guidance, an eligible participant in that age band may be able to contribute more than the standard age 50 catch-up amount. That sounds straightforward until you review an actual payroll process and discover the employer has not updated administration or participant communications.

The less familiar rule is the 15-years-of-service catch-up for certain long-term employees of qualified organizations. The IRS explains that this provision can permit up to $3,000 of additional elective deferrals in a year, subject to a $15,000 lifetime cap and other coordination limits under section 402(g) and section 415(c), as described in IRS Publication 571. This rule is often misunderstood because service history, prior deferral patterns, and plan administration all matter.

That is the point where careful advisors slow the conversation down. A teacher may say, “I'm over 50, so I get the catch-up.” A hospital chaplain may say, “I have 20 years in, so I get the service catch-up too.” Sometimes both are directionally right. Sometimes one of those assumptions fails after document review.

For clients evaluating payout options as retirement nears, the tax character of accumulated assets can also affect income planning alongside annuity decisions, including questions addressed in Kons Law's guide to SPIAs.

How traditional and Roth treatment differ

Tax treatment looks simple on a chart, but advisory judgment sits in the gray areas. Traditional 403(b) deferrals generally reduce current taxable income. Designated Roth deferrals are made with after-tax dollars, with qualified distributions later coming out tax-free.

The planning question is rarely just “taxes now or taxes later.” Advisors should test the choice against expected pension income, Social Security timing, charitable intent, future required minimum distribution exposure, and the client's likely need for flexible taxable income in retirement. A university professor with a pension and large pre-tax balances may need a very different deferral mix than a younger nonprofit physician still in a high-growth phase.

There is also a new compliance angle for high earners. Beginning in 2026, participants whose prior-year wages from the employer exceed the applicable threshold for SECURE 2.0 Roth catch-up treatment may have to make catch-up contributions on a Roth basis if they want to make catch-up contributions at all, assuming the plan offers catch-ups. For advisors, this turns Roth from a planning preference into a payroll and document review issue. If the plan has not been updated operationally, the client can receive incomplete or inaccurate guidance.

A practical recommendation framework looks like this:

- Use traditional deferrals when current-year tax reduction is the priority and future taxable income is expected to be lower.

- Use Roth deferrals when the client can absorb current tax cost and expects meaningful taxable income in retirement.

- Use a split approach when future income visibility is limited or the client needs tax diversification across account types.

- Check high-earner catch-up treatment for 2026 before finalizing deferral elections for clients near or above the wage threshold.

Clients often arrive with a number in mind. Advisors need the rule set behind the number. That distinction is what keeps 403(b) advice accurate, defensible, and suited to the plan in front of you.

Investment Structures Annuities and Custodial Accounts

A school employee brings you two 403(b) statements before retirement. One reads like an insurance contract. The other looks like a mutual fund account. The client wants to know which one is the “real” 403(b). The right answer is both, and that is where many advisor mistakes begin.

Why older 403(b) accounts often look different

403(b) plans began as annuity-based arrangements, which is why many long-tenured participants still hold contracts issued years ago. Congress later expanded the structure to allow custodial accounts invested in mutual funds under 403(b)(7). The result is a plan type with two very different wrappers, both valid, both common, and both easy to misread if an advisor focuses only on the fund lineup.

That history still shows up in current client files. Public school and nonprofit participants often accumulated assets through older enrollment practices, sometimes across several providers. What looks like one retirement account on a household balance sheet may instead be a stack of separate contracts, each with its own transfer rules, fee schedule, death benefit terms, and distribution procedures.

For advisors, that distinction matters because the wrapper can control the client experience as much as the investment allocation does. A low-cost fund inside a restrictive contract can create planning friction. A higher-cost annuity can still have value if the guarantees, surrender schedule, and distribution terms fit the client's needs and are fully understood.

What advisors should evaluate in practice

Start with the legal container, not the performance report. A 403(b) review works much like inspecting the plumbing before judging the water pressure. If you do not know whether the assets sit in an annuity contract or a custodial account, it is hard to give reliable advice on costs, exchanges, liquidity, beneficiary treatment, or rollover timing.

A practical review usually sorts the account into one of these categories:

- Annuity-based arrangement: Often governed by insurance contract provisions, with product-specific withdrawal terms, riders, surrender charges, and exchange restrictions.

- Custodial account arrangement: Often built around mutual funds and easier for clients to recognize, but still subject to plan-level distribution and transfer rules.

For annuity-heavy accounts, a useful educational supplement can be Kons Law's guide to SPIAs, especially when a client is confusing an accumulation annuity inside a retirement plan with an income annuity used later in retirement.

A 403(b) review should ask “what owns the investments?” before it asks “how did the funds perform?”

That question gets more important in multi-vendor school systems. Advisors should check for duplicate providers, stale salary deferral elections, overlapping asset allocations, and contract-level limits on transfers or exchanges. Those details often drive the compliance and planning work. They affect rollover execution, required paperwork, liquidity assumptions, and whether the participant can realistically consolidate accounts without triggering avoidable costs or delays.

This is also where stronger 403(b) advice separates itself from generic retirement plan advice. The issue is not just annuity versus mutual fund. The issue is whether the advisor has identified the governing structure, read the contract language, and matched recommendations to the actual administrative rules the client is living under.

403(b) vs 401(k) A Strategic Comparison for Client Planning

Clients ask this comparison because they want to know whether their plan is better, worse, or different. Advisors should answer in terms of planning consequences, not product prestige.

403(b) vs. 401(k) At a Glance

| Feature | 403(b) Plan | 401(k) Plan |

|---|---|---|

| Eligible employers | Public educational institutions and eligible tax-exempt organizations | For-profit employers |

| Typical historical structure | Often shaped by annuities and custodial accounts | Commonly built around broader corporate plan menus |

| Special catch-up feature | May include a long-service catch-up under the 15-year rule if the plan permits | No equivalent long-service rule discussed here |

| ERISA status | Can be ERISA or non-ERISA depending on employer and plan structure | Commonly treated as an ERISA-governed workplace plan |

| Client planning focus | Vendor cleanup, legacy contracts, long-service review, Roth catch-up nuances | Employer match structure, menu design, rollover sequencing |

For a concise outside perspective that many advisors may find useful in client education, NPDiva Consulting's 403(b) insights summarize several practical distinctions in plain language.

Where the planning differences show up

The biggest mistake is treating the comparison as an academic exercise. It's more useful when applied to household decisions.

Consider a couple where one spouse works in public education and the other in the private sector. The advisor may need to coordinate contribution strategy across a 403(b) and a 401(k), review whether one account offers more attractive Roth flexibility, and decide which balance is the better rollover candidate after retirement or separation.

A few planning distinctions matter repeatedly:

- Employer identity drives plan type: Clients don't choose between a 403(b) and 401(k) the way they choose a fund.

- Legacy plan baggage can be heavier in 403(b)s: Older contracts and multiple vendors often require more document review.

- Catch-up analysis can be more nuanced in 403(b)s: Long-service eligibility and age-based tiers can create planning opportunities or confusion.

- Rollover advice may differ: Contract restrictions, annuity features, and employer-specific rules can all affect the recommendation.

Some advisors overstate the distinction and make the 403(b) sound exotic. It isn't. But it does require sharper file review and more careful assumptions than many retail summaries suggest.

Navigating Distributions Rules for Withdrawals and Rollovers

A client leaves a university job, brings in a stack of old 403(b) statements, and asks one question: “Can I just move this to my IRA next week?” That is often the moment where basic product knowledge stops being enough. Distribution advice in a 403(b) requires timing checks, contract review, and careful tax sequencing. For advisors, the risk is not just giving an incomplete answer. The risk is approving a transaction that creates avoidable tax, misses an RMD, or moves assets that were not eligible to roll.

Withdrawal timing matters more than clients expect

Two rules drive many mistakes.

First, required minimum distributions begin once the participant reaches the applicable starting age under current law, and the penalty for failing to take the full amount can be severe. The IRS explains the excise tax framework for missed RMDs in its guidance on retirement plan and IRA required minimum distributions FAQs. Advisors should not assume the recordkeeper, employer, or annuity issuer has handled the calculation correctly, especially when a client has changed employers, holds multiple contracts, or has legacy balances spread across vendors.

Second, early distributions usually mean ordinary income tax and may also trigger an additional tax before age 59½ unless an exception applies. That sounds straightforward until a client asks about severance, disability, hardship, plan loan offsets, or a contract-based restriction that limits access even when the tax code would permit a payout.

Available is not the same as prudent.

A strong review starts with the facts the statement does not show clearly. Has the client separated from service? Is the account still inside the employer plan, or sitting in an individual annuity contract under the 403(b)? Is any portion already subject to distribution requirements? Those details change the recommendation.

Rollovers require more than a transfer form

Advisors often treat rollovers as an administrative clean-up project. In 403(b) work, that approach can miss the core issue. The question is whether the rollover improves the client's position after accounting for surrender terms, investment menu changes, creditor considerations, beneficiary planning, and near-term income needs.

A practical file review should usually cover:

- RMD status: Confirm whether any amount must be distributed before a rollover can occur.

- Source of assets: Separate pre-tax money, Roth deferrals, and any after-tax amounts so the destination account matches the tax character.

- Contract terms: Review surrender charges, annuity income riders, transfer limitations, and employer-specific distribution procedures.

- Trigger for eligibility: Verify whether the client has a distributable event rather than assuming age or job change alone settles the issue.

- Household planning context: Compare the 403(b) move against pension income, IRA balances, emergency reserves, and the client's expected withdrawal sequence.

For broader context on how withdrawal rules can evolve across workplace plans, Allied Tax Advisors' insights on 401k withdrawals can help frame client conversations about why plan-specific details matter before money leaves the account.

This is also a process discipline issue inside the advisory firm. Teams that document plan type, distribution triggers, contract features, and rollover recommendations in a consistent intake workflow tend to give cleaner advice and catch more exceptions. A structured client relationship management process for financial services firms helps preserve those details when a case involves multiple legacy 403(b) accounts and several decision points.

The advisor's job is to slow the transaction down long enough to test the assumptions. In 403(b) distribution work, that pause often prevents the error the client never knew was possible.

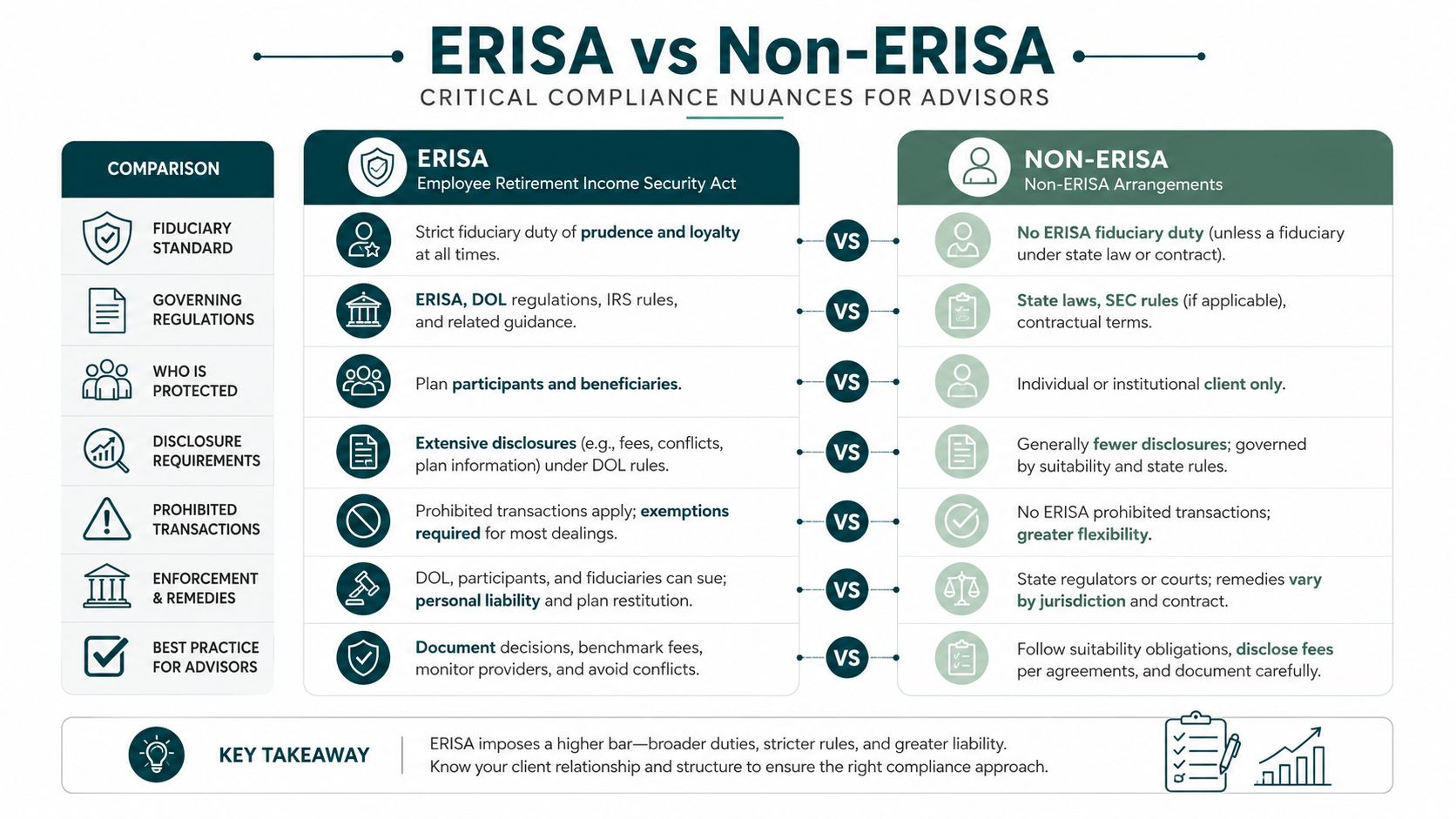

ERISA vs Non-ERISA Critical Compliance Nuances for Advisors

A new 403(b) client walks in with two old contracts, current salary deferrals, and a simple question about next year's savings strategy. The recommendation looks straightforward until you identify the key threshold issue. Is this an ERISA plan or a non-ERISA church or public school arrangement? That single fact changes the compliance frame for nearly everything that follows.

Why ERISA status changes the advisory conversation

Advisors often begin with contribution limits or investment menus. In 403(b) work, governance usually deserves attention first. Public school 403(b) plans are often outside ERISA, while many nonprofit arrangements fall under ERISA unless a regulatory exemption applies. Church plans add another layer and should never be classified by habit.

That distinction affects who is responsible for oversight, what participant protections apply, how disclosures are handled, and how much employer involvement exists in plan operation. A participant statement will not tell you all of that. The file has to.

A sound intake process should document employer type, plan sponsor involvement, the number of vendors, and the governing plan materials. Firms that want fewer avoidable errors usually benefit from a documented client relationship management process for financial services firms that preserves those details from first meeting through recommendation.

A few questions should appear early in the review:

- Is the arrangement ERISA, non-ERISA, or potentially a church plan? Each category changes the compliance analysis.

- Who controls eligibility, loans, hardship approvals, and distributions? Administrative authority often reveals how the plan operates.

- How many vendors or legacy contracts are still tied to the plan? Multiple providers can obscure contribution history and account restrictions.

- Is there a current written plan document or coordinated written program? For 403(b) plans, that is a foundation issue, not paperwork trivia.

The written plan point deserves special attention. IRS guidance makes clear that a 403(b) plan must be maintained pursuant to a written plan that satisfies the applicable requirements in both form and operation. If the written program is weak, outdated, or not followed in practice, the risk is not theoretical. It can affect plan qualification and create correction exposure that the advisor may be the first person to spot. See the IRS 403(b) Fix-It Guide for the agency's discussion of the written plan requirement and operational failures: https://www.irs.gov/retirement-plans/403b-fix-it-guide

The 2026 Roth catch-up issue advisors cannot miss

Another compliance point is easy to miss because clients still frame catch-up contributions using old assumptions. Beginning in 2026, catch-up contributions for higher-wage participants generally must be made on a Roth basis if the participant's prior-year FICA wages from that employer exceed the statutory threshold. For advisors, the practical issue is not the headline rule. It is whether payroll, plan design, and client expectations are aligned before year-end elections are set.

A pre-tax projection can fail quickly here. If a senior employee expects to increase deferrals and reduce current taxable income, but catch-up dollars must go into a designated Roth source, the tax outcome changes. So does withholding strategy. So can the client's willingness to maximize deferrals.

This tends to surface with nonprofit executives, hospital administrators, and late-career professionals trying to accelerate savings. Before finalizing a recommendation, confirm three things. Whether prior-year wages cross the threshold. Whether the plan supports Roth catch-up contributions operationally. Whether the client understands that the catch-up amount may no longer reduce current taxable income. IRS guidance on SECURE 2.0 catch-up treatment provides the governing framework advisors should review with payroll and plan contacts: https://www.irs.gov/retirement-plans/plan-sponsor/secure-20-act-changes-to-catch-up-contributions

The broader lesson is simple. In 403(b) planning, the advisor who identifies plan status and operational compliance early will usually give better advice than the advisor who starts with product selection or contribution math alone.

Frequently Asked Questions from Financial Advisors

How should an advisor handle a client with multiple 403(b) accounts from different vendors

Start with inventory, not recommendations. Gather every statement, beneficiary record, contribution history note, and contract summary available. Then identify which accounts are active, which are legacy, and which contain restrictions that could affect transfers or future distributions.

Consolidation may help, but only after the advisor reviews tax character, investment structure, and any contract-specific features. A scattered 403(b) household can still contain one account that should remain untouched and another that clearly warrants cleanup.

What are the first questions to ask a new 403(b) client

The most useful opening questions are practical:

- Who is the employer? That helps frame eligibility and likely governance structure.

- Is the client still contributing? Active salary deferrals change the planning discussion.

- Does the plan offer Roth contributions? This becomes critical for tax planning and catch-up strategy.

- Are there old contracts or multiple vendors? Those details often reveal hidden complexity.

- Has anyone reviewed the contribution ceiling recently? The combined employer and employee contribution cap for 2026 is $72,000, not including catch-up amounts, according to the University of California 403(b) summary plan description.

When does a 403(b) review become a compliance issue instead of just an investment review

It becomes a compliance issue when the advisor gives guidance without understanding plan status, written plan terms, catch-up eligibility, distribution timing, or tax treatment. Those aren't side notes. They shape whether the recommendation is accurate.

The cleanest approach is to treat every 403(b) file as a document-review assignment first and an allocation discussion second. That keeps the advice anchored to the actual rules governing the client's account.

Financial advisors who want sharper content, stronger digital positioning, and compliance-aware growth support can explore Advisor Momentum. The firm works exclusively with advisors, planners, and banking professionals on branding, websites, content, advertising, coaching, and recruiting built for regulated financial businesses.